Oil:

- Oil rebounds at the start of the new week due to geopolitical concerns. Biden has authorized Ukraine to use long-range missiles to attack positions in Russia

- Investors are concerned that Ukraine will target Russian oil infrastructure to cut off the country from its main source of funding

- Concerns about demand in China next year are leading to forecasts of price drops to $40 per barrel. Chinese refineries processed just over 14 million barrels per day in October, almost 5% lower than last year

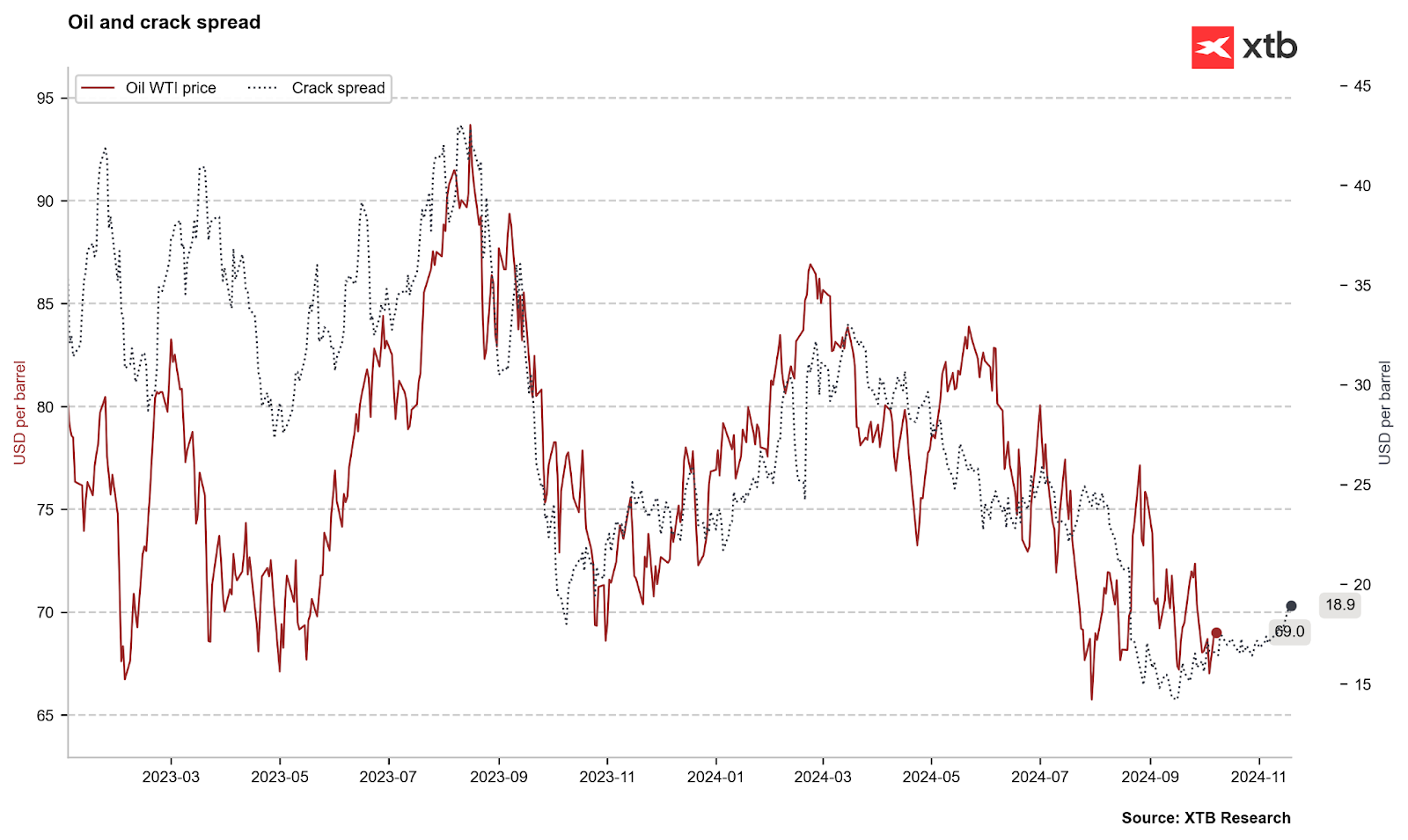

- US refineries are trying to work at double capacity. Recently, we’ve observed a clear rebound in the crack spread, suggesting that the potential short-term bottom may be behind us

- Although prospects for next year appear mixed, with significant supply uncertainty, we’re observing the beginning of closing divergence between WTI oil and TNOTE (inverse)

Crack spread suggests that the local bottom in oil may be behind us. A similar situation is also occurring in the differences between nearest contracts, although recent spread declines may indicate curve inversion, suggesting possible further declines next year. Source: Bloomberg Finance LP, XTB

Oil rebounds and currently might be forming a double/triple bottom pattern. The formation range would indicate even $79 per barrel. Meanwhile, uniform divergence closure would indicate oil price increases to $75 per barrel. Currently, key resistance levels are $70 (half the distance between 25 and 50 averages), followed by $73 along with the 100-period average. Source: xStation5

Gas:

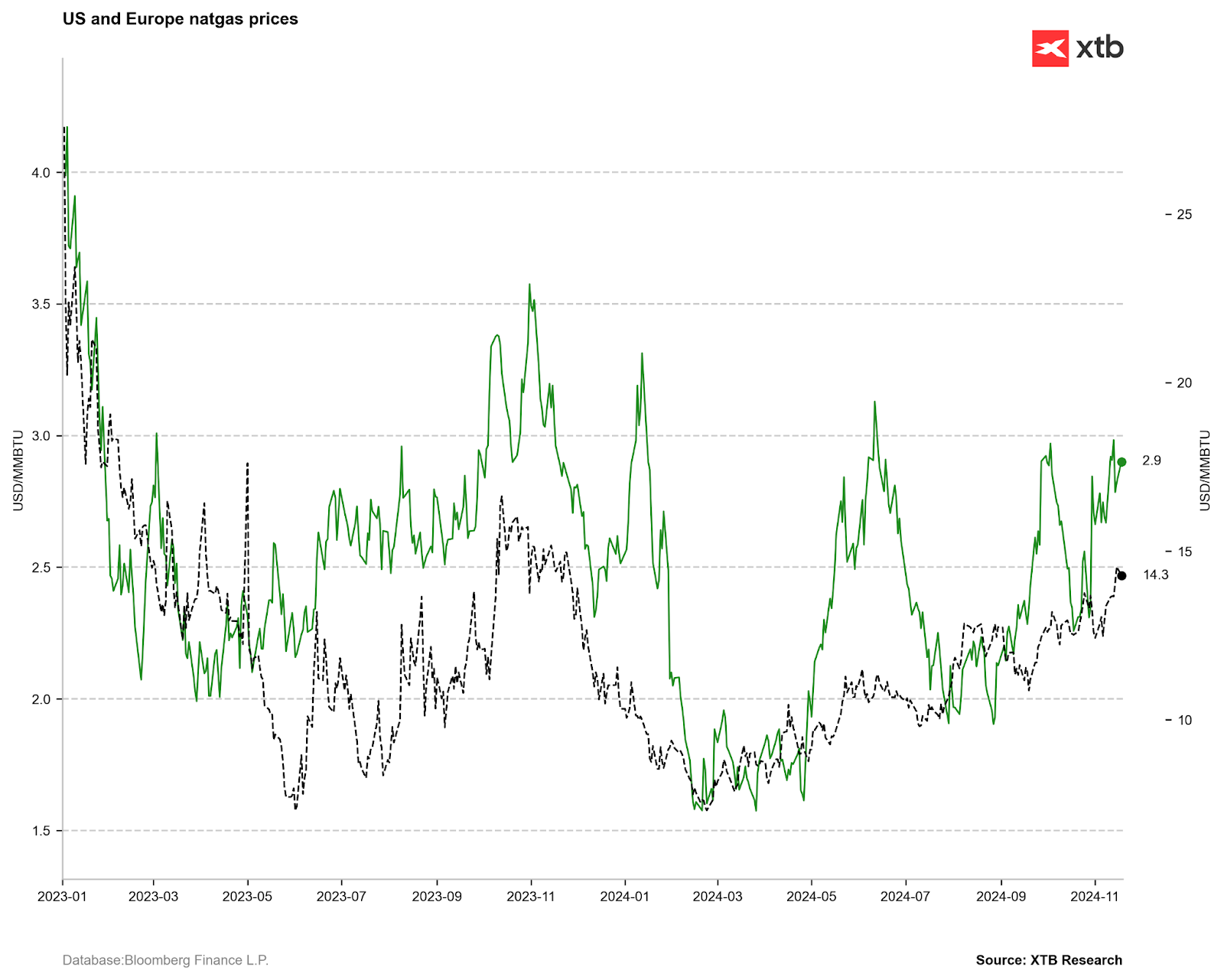

- Gas prices in Europe and the US remain at elevated levels

- European gas prices are rising due to freezing weather and higher-than-usual gas usage

- Russia is also informing Austria that it intends to halt gas supplies through the pipeline running through Ukraine soon. Russia plans to continue pipeline deliveries to Hungary and Slovakia

- Weather conditions in the United States remain stable, but recently there has been a decrease in production and exports

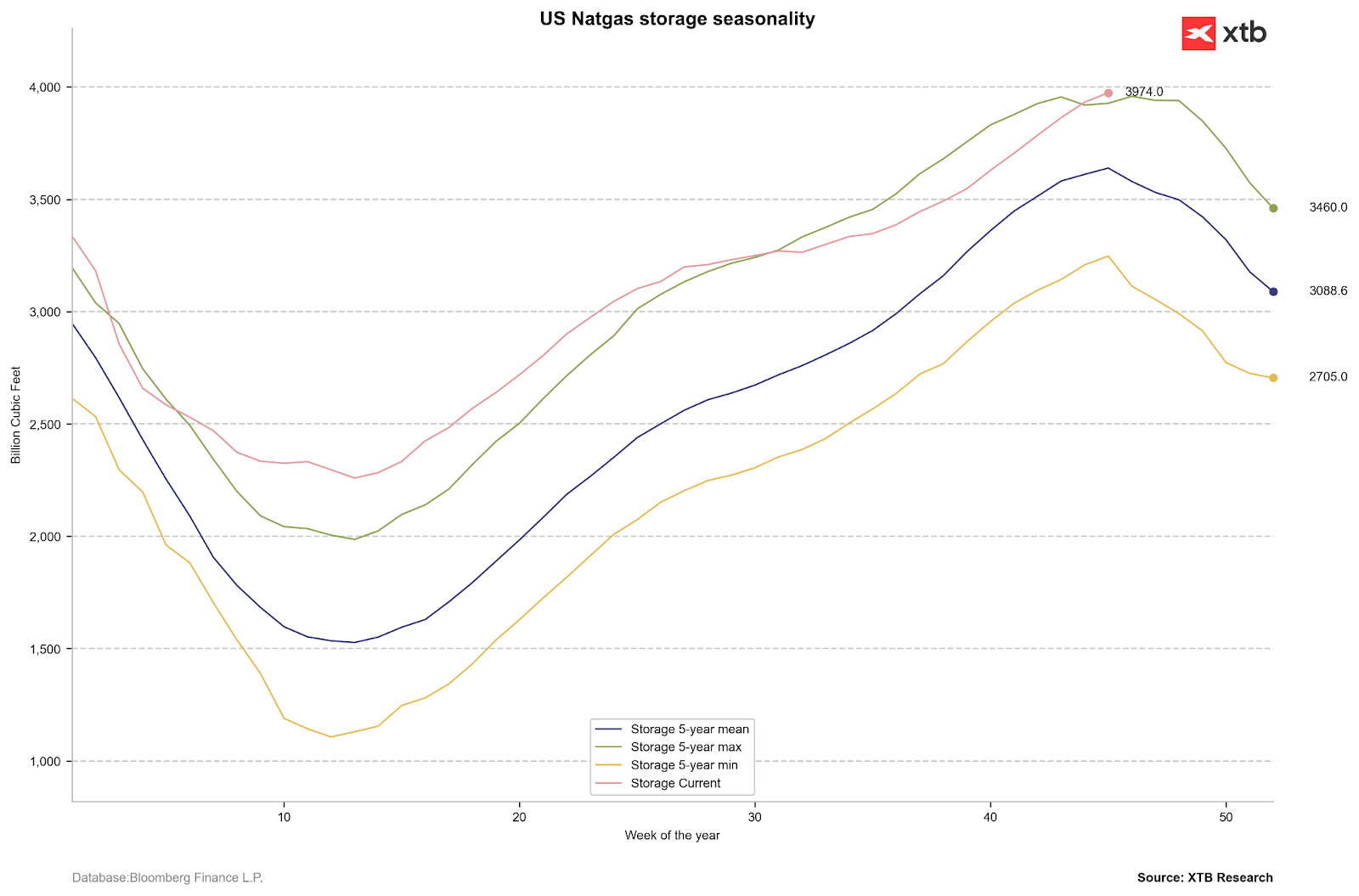

- Gas inventories continue to rise in the US. However, the seasonal decline in inventories is approaching

US inventories remain at their highest level in 5 years, despite production issues. Lack of change to cold weather may cause inventories to start declining later than in the last 5 years. Source: Bloomberg Finance LP, XTB

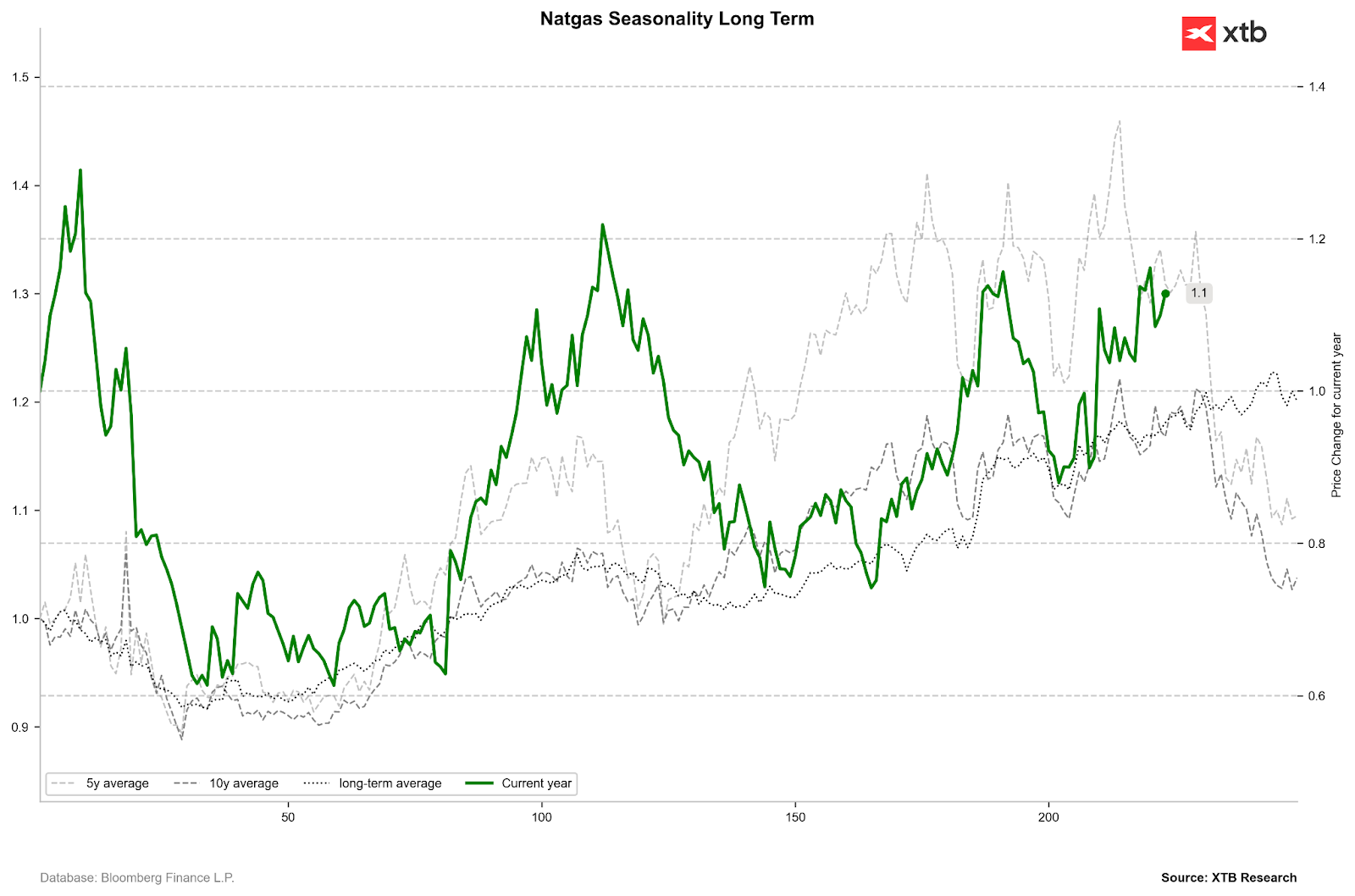

Gas prices deviate from seasonality, but 5 and 10-year seasonality indicates declines in the second half of November and December. Long-term seasonality indicates consolidation in December. Source: Bloomberg Finance LP, XTB

Gas prices in the US and Europe remain at elevated levels. However, looking at price behavior in Europe last year, significant declines began in the second half of November. Currently, the forward curve in Europe remains in slight backwardation from the perspective of nearest months. In the US, one more positive rolling is expected. Source: Bloomberg Finance LP, XTB

Contract rolling will take place in two days. The oil price remains at elevated levels and responds to the upward trend. The price after rolling could potentially exceed peaks from the first half of June at $3.1/MMBTU. Source: xStation5

Gold:

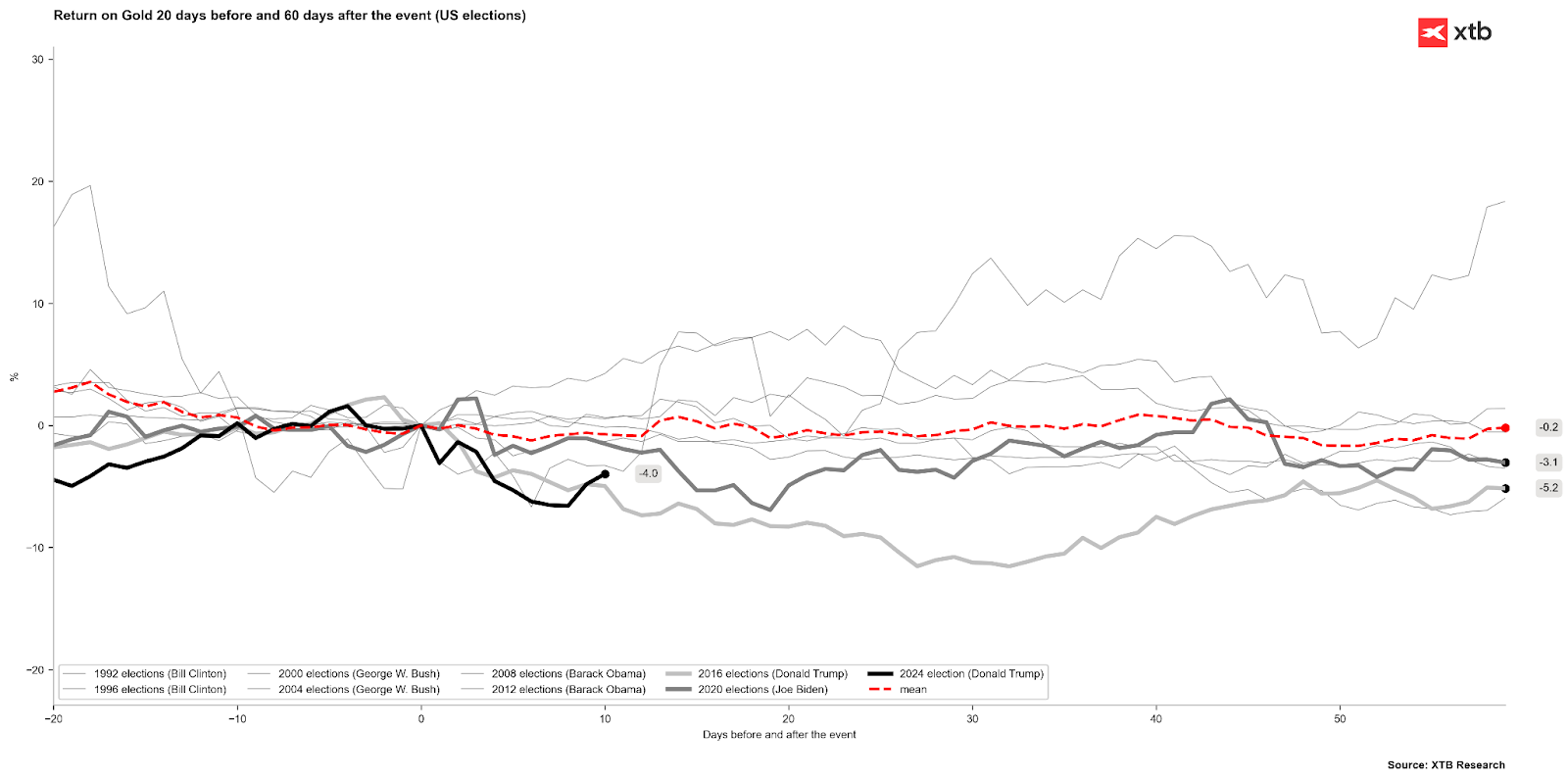

- Gold rebounds for the second consecutive day, and in the first session of the week, the downward streak that had occurred almost continuously since the US presidential elections ended

- Price behavior after elections in 2016 and 2020 suggests maintenance of declines 20-30 sessions after elections, but declines then did not exceed 10%

- Declines since elections have not exceeded 8%, while from the end of October they reached maximum 9%

- Currently, there’s talk primarily about significant jewelry demand in India, but simultaneously, data from this year shows a double-digit decline in jewelry demand in China. This trend may continue next year

- The price should potentially reach a local bottom next week. The current rebound target could be around $2670 per ounce, where there’s a 50.0 retracement of the last downward wave and 23.6 of the upward impulse ongoing since June. The 50-period average and local peaks from September 26 are also located here

Source: xStation5

Gold has significantly limited losses in the last two sessions. Source: Bloomberg Finance LP, XTB

Cocoa:

- After November’s futures contract rolling, significant uncertainty emerged regarding current supplies and those in coming weeks

- Most deliveries to Ivory Coast ports are expected in the next 4-5 weeks, while excessive rains in some areas may cause significant mold problems

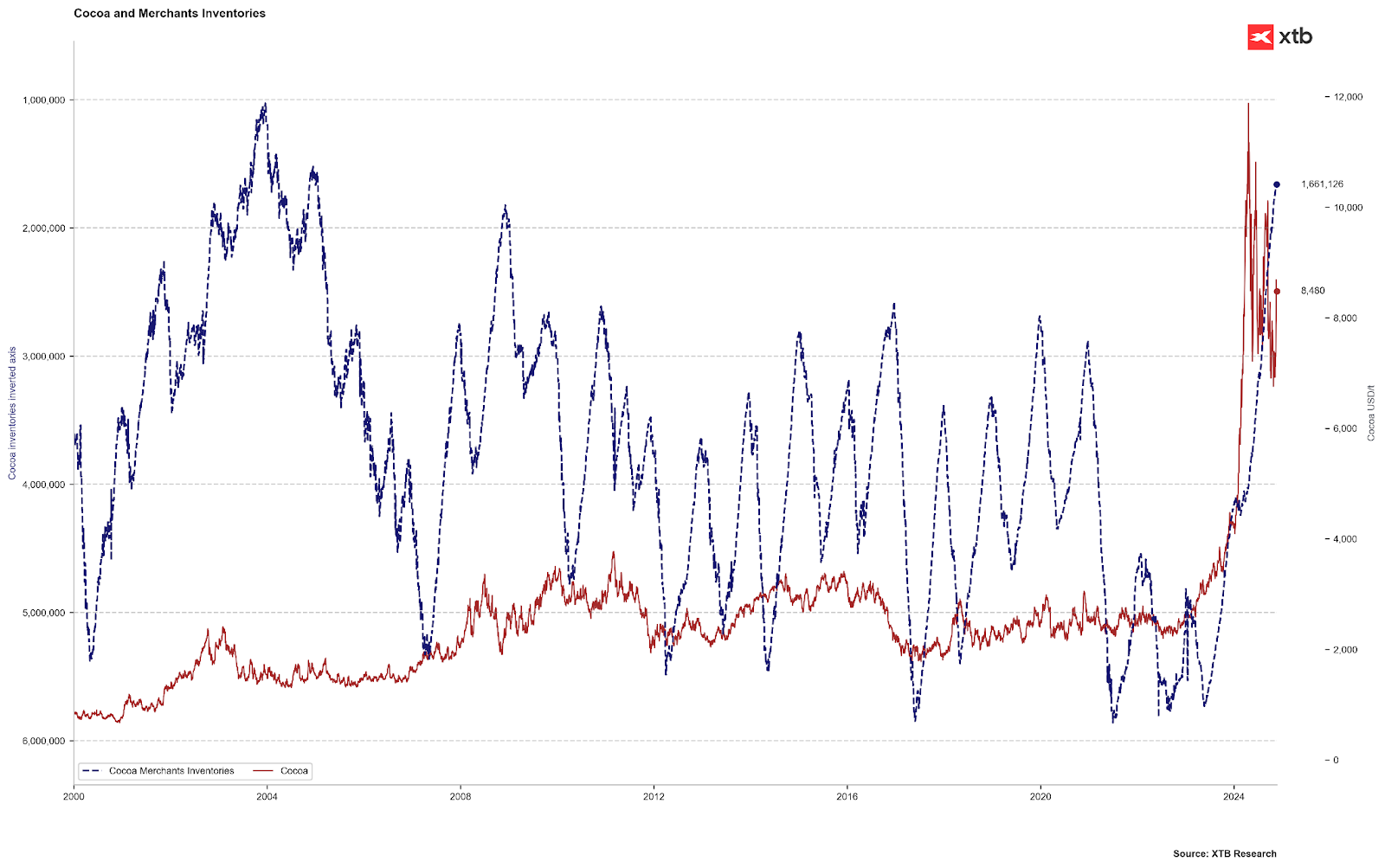

- Low cocoa quality will cause exchange inventories not to rebound. These continue to fall, even despite higher deliveries to ports than last year

- The Ivory Coast regulator allows export of cocoa with 80 to 100 beans per 100 grams (with small deviations in both directions). Currently, the average number of beans delivered to ports per 100 grams is 105, potentially indicating lower quality (smaller beans)

- However, the price experienced a small correction at the turn of the previous and current week, which is related to reduced pressure regarding European regulations

- ICE indicates that it’s delaying changes regarding cocoa and coffee futures contracts due to delayed implementation of deforestation regulations in the European Union. New regulations were supposed to take effect at the end of this year

- Potentially new regulations caused lower available cocoa supply for the European market, which is the largest in the world for this commodity

- Cocoa deliveries to Ivory Coast ports totaled 548,000 tons from October 1 to November 17, which is 32% higher than last year’s level of 415,000 tons

- Maxar Technologies indicates that dry weather and high temperatures in Ghana and Nigeria may again affect production limitation in the so-called Mid-season, which begins at the turn of April and May

Cocoa inventories continue to decline and are at their lowest level since May 19. Source: Bloomberg Finance LP, XTB

Breaking the price of 8700-9000 would likely result in an attempt to reach around 10000 USD. On the other hand, there are concerns about demand at such high prices. If processing data for Q4 comes in weak (and potentially this is the best quarter of the year), it will mean we’re dealing with demand destruction. Source: xStation5

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.