Oil:

- OPEC+ has indicated in its latest statement that it intends to proceed with increasing production from April.

- The production increase is intended to offset the voluntary reduction of 2.2 million barrels per day over several months.

- WTI crude oil prices are hovering below $67.5 per barrel, their lowest level since the first half of December.

- Trump’s decision to impose tariffs on Canada, Mexico, and additional levies on China may, in the long term, lead to a reduction in international trade and thus decrease demand for crude oil.

- The United States is imposing a 10% tariff on crude oil from Canada, which will have a limited impact on reducing oil imports from Canada.

- The current difference between WTI and Canadian WCS crude oil is $13, but it has been higher in the past, indicating the possibility of price adjustments to the new realities of the trade war.

- Increased expectations of peace in Ukraine may also put pressure on oil prices due to potentially easier access to the Russian market if some US sanctions are lifted.

WTI crude oil is testing the $67 per barrel level. This zone has been tested five times between September and December 2024. Oil also traded in this zone in 2023. The next key technical support level is around $62 per barrel, the local lows from 2021. At the same time, we are observing a clear reduction in long speculative positions in WTI crude oil recently, although we cannot yet speak of extreme overselling, as was the case in September 2024, or in the previous two years. Source: xStation5.

Gold:

- Uncertainty regarding the trade war and peace in Ukraine is driving a resurgence in the gold market. At this moment, it is only 1.5% away from historical highs.

- In the US, we are observing a significant drop in yields and a weakening of the US dollar. The market partly hopes that the trade war will be short-lived.

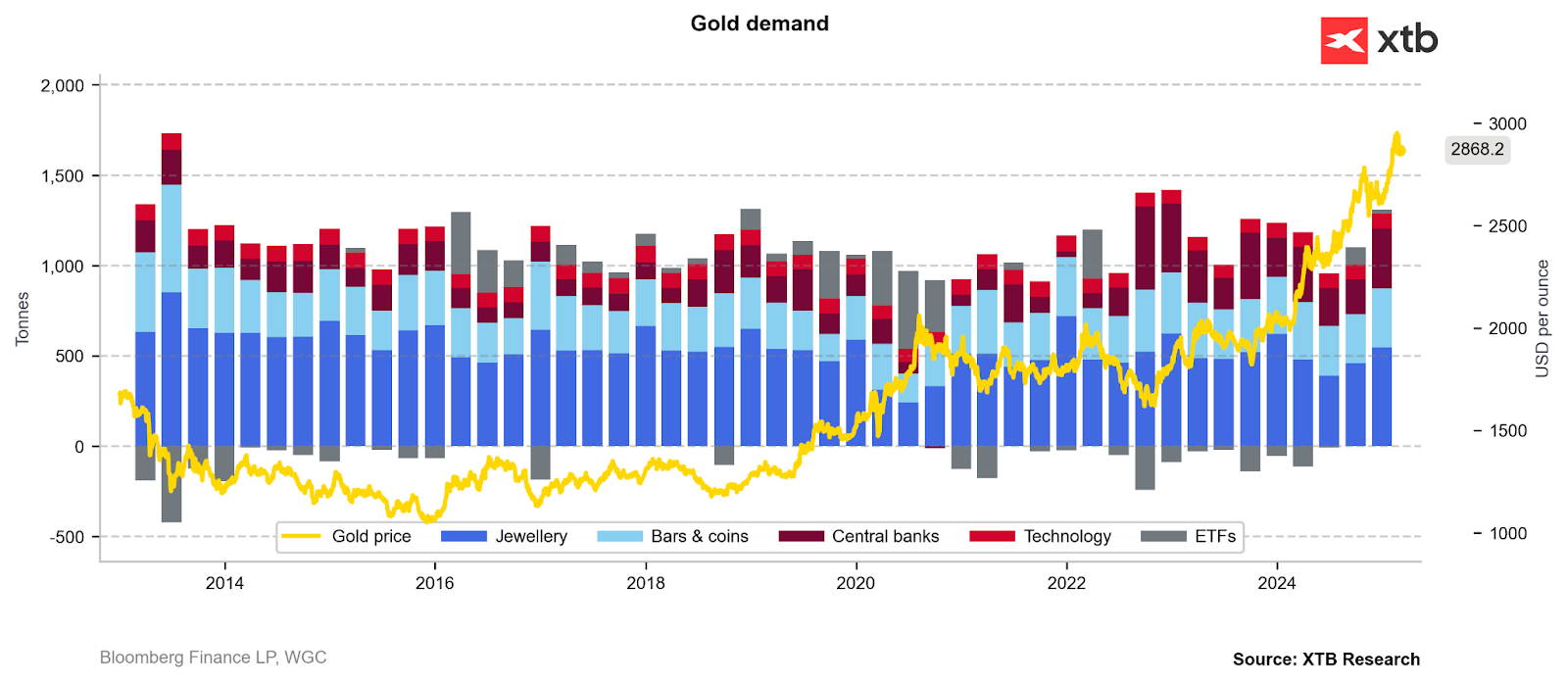

- The latest WGC report on gold fundamentals showed a minimal surplus in the fourth quarter of 2024 of 20 tons of gold. This is due to a significant rebound in jewelry demand and solid demand from central banks and investment demand.

- The balance sheets of the four largest central banks have been rebounding since the beginning of January, which is also a factor supporting high gold prices.

- In the near future, the United States will have to roll over a very large amount of debt, which could potentially lead to a decrease in demand for gold.

- Inventory levels on COMEX are already reaching the levels of the 2020 peak, when, due to fears of COVID, a very large amount of gold was also brought to the US from Europe.

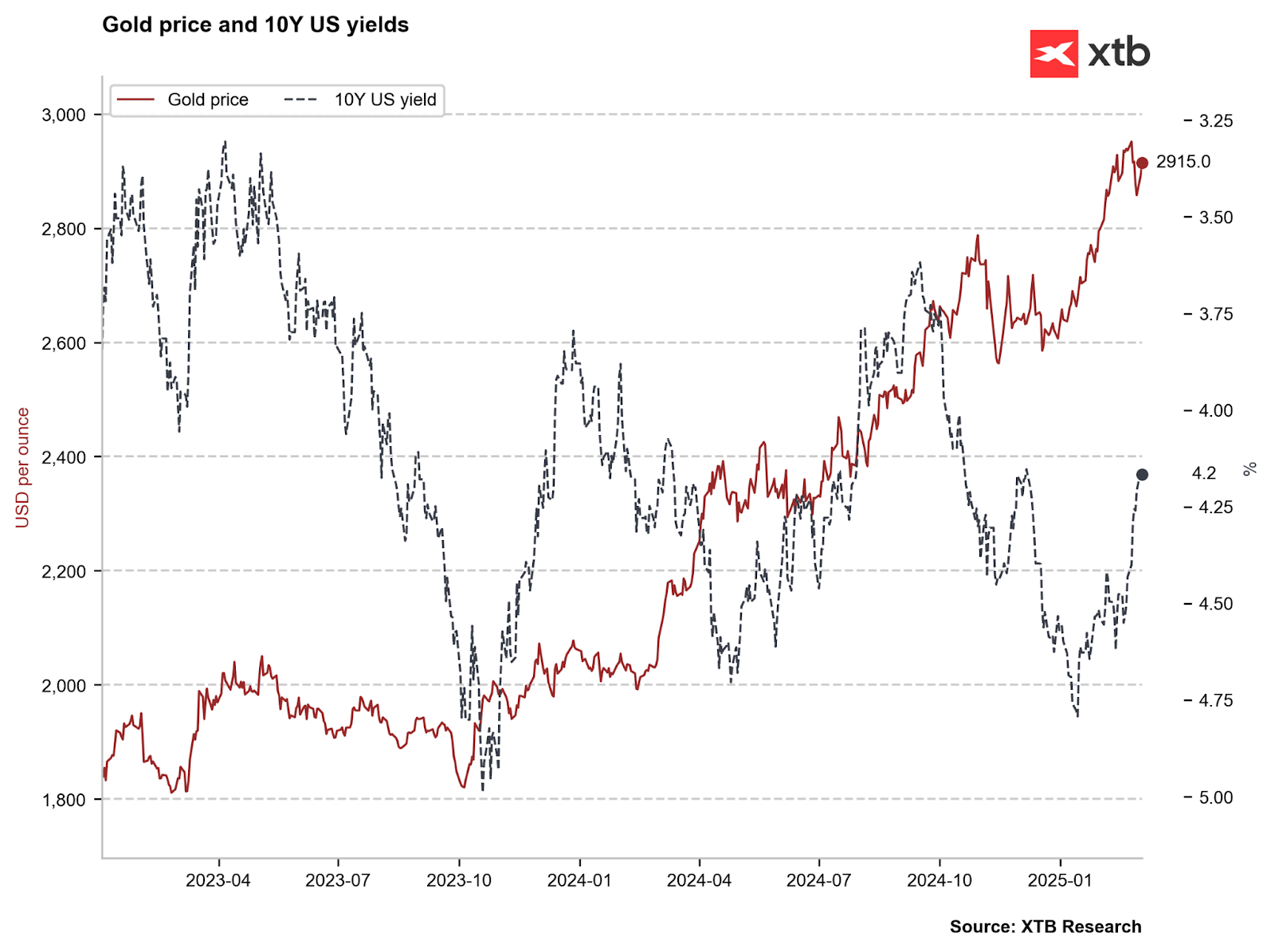

US yields have fallen significantly recently, which is a factor supporting the recent gold rally. Source: Bloomberg Finance LP, XTB.

The end of 2024 brought a clear revival in demand, both in the jewelry sector and from central banks. Source: Bloomberg Finance LP, XTB.

Gold has gained nearly 10% this year, while the S&P 500 is down about 2% this year. The recent sharp pullback in the stock market caused a pullback in gold due to the search for liquidity, but without a crash, the situation in the gold market should stabilize. Source: xStation5.

Natural Gas:

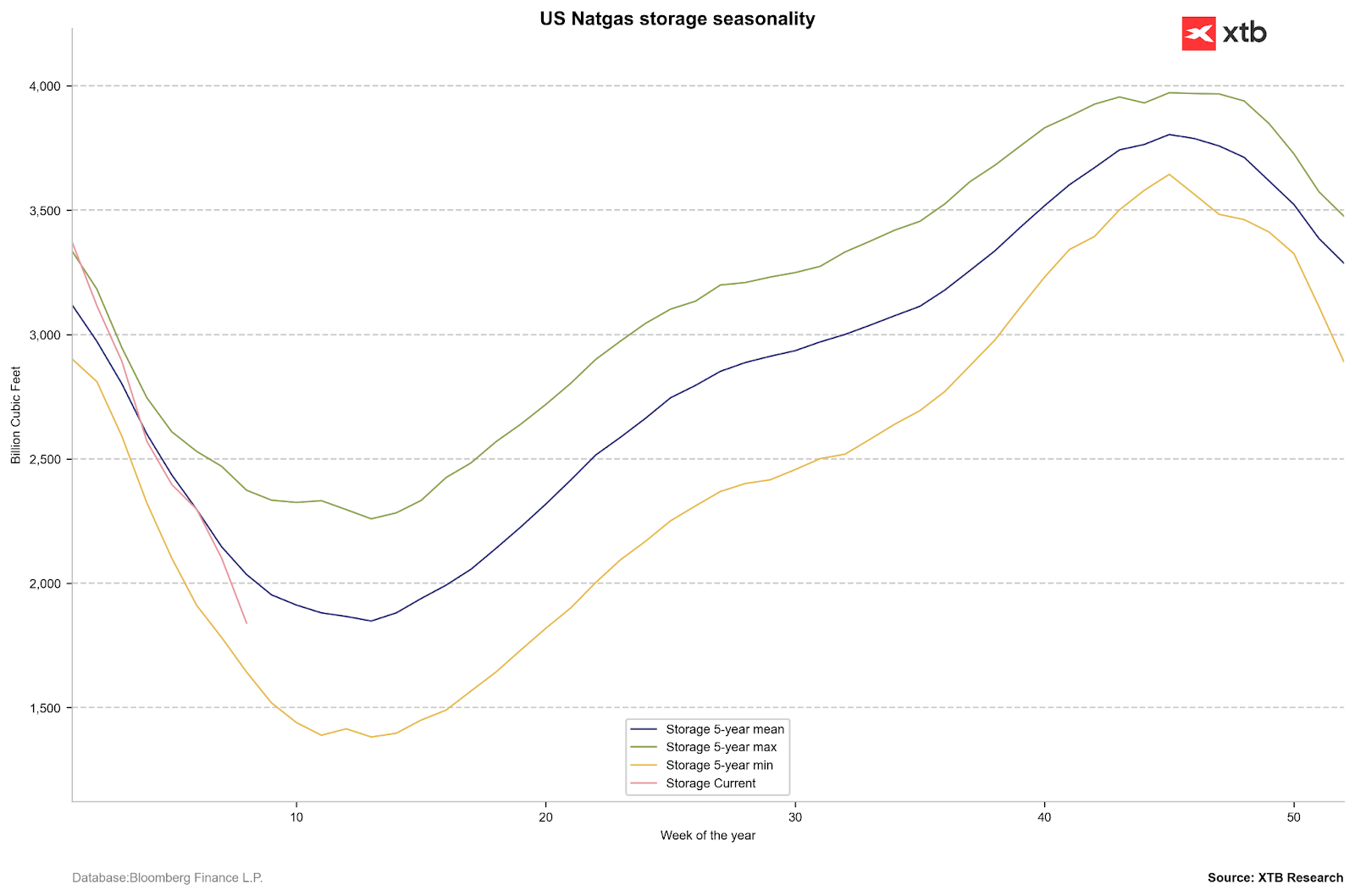

- US gas inventories remain significantly below the 5-year average, but the coming weeks should bring minimal inventory declines, while the first inventory replenishments may be possible in early April, depending on the weather.

- Current forecasts indicate significantly higher temperatures in the coming weeks than standard, which should reduce gas consumption for heating purposes.

- On the other hand, the US is currently sending record amounts of LNG, which, of course, suggests that rebuilding inventories in the near future will be more difficult than in previous years, without a significant increase in production, which currently still hovers near 105 bcfd.

- The price increase in the market since the beginning of the first week of March was also driven by the imposition of trade tariffs on Canada, which could potentially increase demand for US gas locally.

- Currently, LNG shipments averaged in March at 15.8 bcfd.

US gas inventories remain significantly below the 5-year average. In the next 2-3 weeks, we should observe a further decline in inventories, although probably at minimal levels. The further fate of prices will depend on the rate of inventory replenishment in the coming month ahead of the next heating season. Source: Bloomberg Finance LP, XTB.

Natural Gas production is currently at record levels in the US, but with significantly increased exports, this may not be enough to replenish inventories at a sufficient rate. Source: Bloomberg Finance LP, XTB.

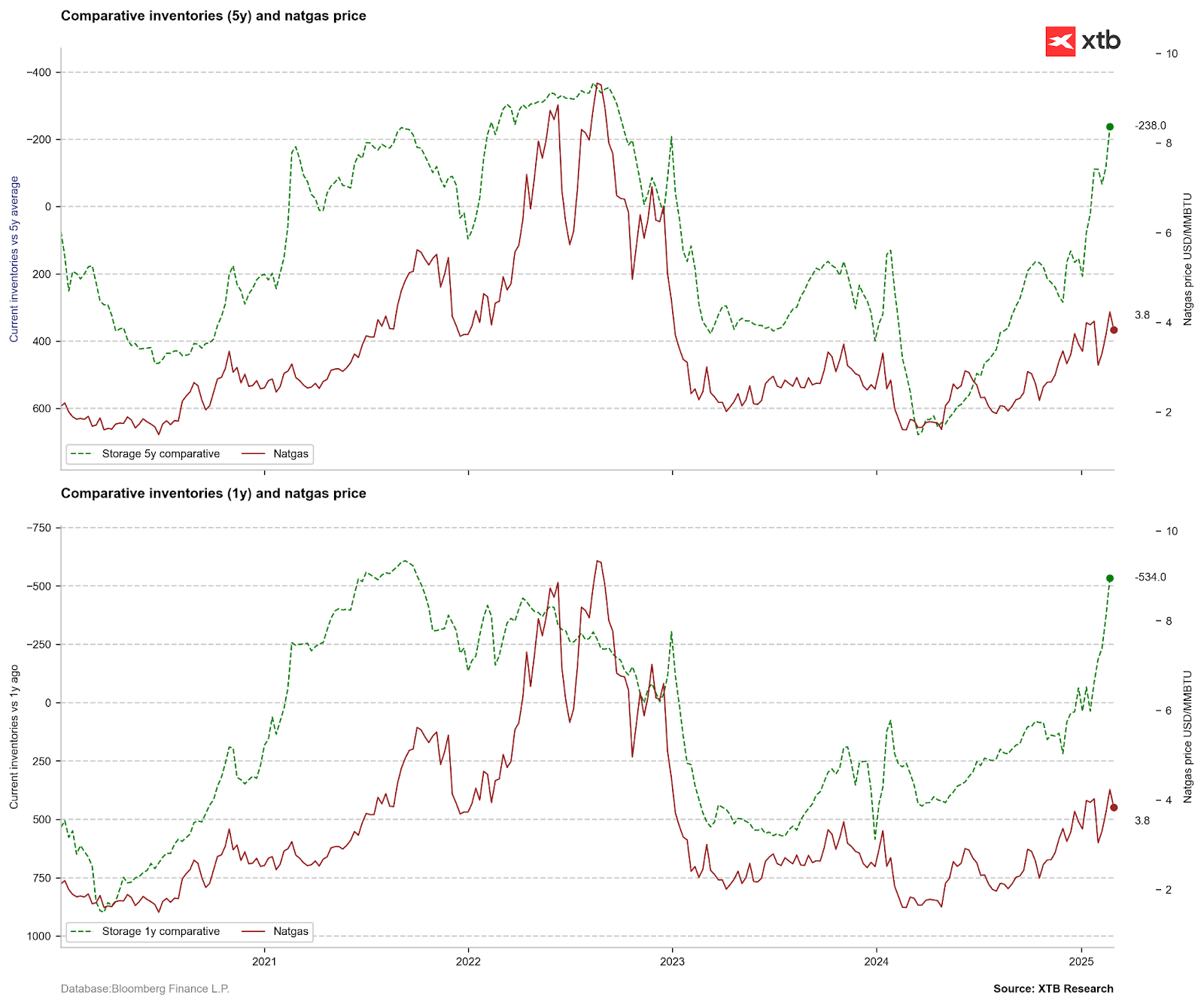

The current situation is beginning to resemble 2021 and 2022, when, after a sharp drop in inventories, we observed the building of potential for a strong price increase in the US gas market. Comparative inventories show that the NatGas market is in significant deficit. Source: Bloomberg Finance LP, XTB.

Gas prices have risen to their highest levels since the beginning of 2023, while prices remain below $4.3/MMBTU. Weather theoretically suggests a potential decrease in gas demand, but prices remain highly volatile. In the event of a reaction to reduced demand, a decline between the 60 and 120 SMA averages may occur. However, if strong demand continues and inventories decline more sharply, an approach to the $4.8-5.0/MMBTU zone is possible. Source: xStation5.

Cocoa:

- Cocoa prices have fallen to their lowest point, down 40% from their historical peak in mid-December 2024.

- The price decline from the beginning of this year to today is approximately 25%.

- The price is maintaining a long-term upward trend line. Additionally, the $7,000 level appears to be a key support for the cocoa market.

- Investors continue to withdraw from the market. Both long and short positions are falling, but the reduction in long positions is stronger. Net positions have fallen to around their lowest level since April 2024.

- The recent sharp price decline was intensified after the release of the ICCO report, which indicates a surplus in the 2024/2025 season of 142,000 tons.

- ICCO indicates a 4.8% year-on-year decline in demand and a 7.8% year-on-year increase in supply. Last year, production fell by 16.4% year-on-year.

- However, the increase in production by ICCO is smaller than the current increase in cocoa deliveries to ports in Ivory Coast, which is approximately 16% (in December, this increase exceeded 30%). This potentially means that ICCO expects a very weak mid-season, which is scheduled to begin in April.

The price of cocoa has rebounded from the level of $8000 per ton, but remains below $9000 and below the 250 session average. These levels may currently represent very important resistance. Without any signs of improvement in demand, it may be difficult to return prices above $10,000 per ton. Source: xStation5.

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.