EUR /

EUR /  USD — Euro / US Dollar

USD — Euro / US Dollar JPY — US Dollar / Japanese Yen

JPY — US Dollar / Japanese Yen GBP /

GBP /  AUD /

AUD /  CAD — US Dollar / Canadian Dollar

CAD — US Dollar / Canadian Dollar CHF — US Dollar / Swiss Franc

CHF — US Dollar / Swiss Franc NZD /

NZD / Alphabet Q1 Preview: High Bar and Pressure on Quality

- April 28, 2026

- Posted by: Today Markets

- Categories: Competitive research, Funding trends, Markets, Technical Analysis

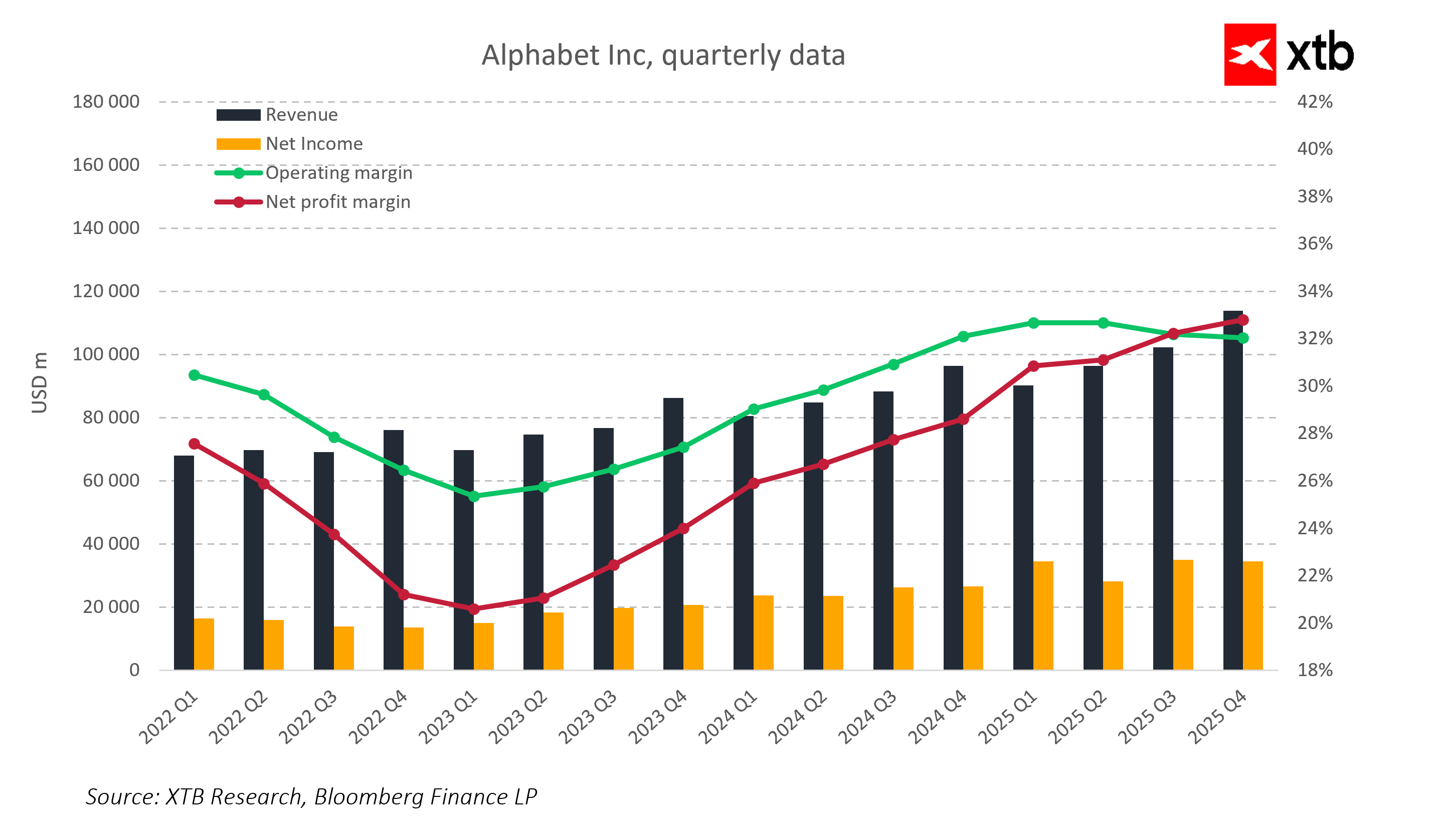

Alphabet enters its Q1 2026 earnings release at a point where the company is no longer priced as a traditional advertising giant, but rather as one of the key beneficiaries of the global artificial intelligence cycle. This shift is changing the way the market interprets every upcoming report, as the focus of evaluation is moving away from revenue growth momentum toward the durability and quality of the entire business structure. In practical terms, this means that even very solid results may fail to trigger a positive market reaction if they do not support the broader narrative of scalable AI adoption and sustained profitability amid heavy investment. Today, Alphabet is expected to simultaneously demonstrate strength in advertising, execution in cloud computing, and genuine monetization of artificial intelligence across its entire product ecosystem. The key market expectations for Q1 2026:

- Revenue of approximately 106.9 billion USD,

- EPS of around 2.7 USD,

- Google Cloud revenue of roughly 18 billion USD with growth of approximately 40–50 percent year over year

- Operating margin near 33 percent

- CapEx remaining at a very elevated level, broadly in line with previous quarters and still driven by investments in AI and data infrastructure.

Market expectations and the bar that has been set

The market is pricing in another quarter of stable revenue growth, with Google Cloud playing a central role alongside continued resilience in the advertising segment. At the same time, investors remain fully aware that the company is still in a phase of very intensive investment in AI infrastructure, which naturally limits near-term visibility on full profitability of these initiatives. Against this backdrop, what matters is not only whether Alphabet meets consensus expectations, but also how growth is distributed across segments and whether a balance is maintained between the scale of investment and improvements in operational efficiency. The market is demanding not just growth, but growth of the right quality.

Google Cloud and artificial intelligence as the core narrative Google

Cloud remains the most important element of Alphabet’s investment story and the primary source of potential re-rating. The focus is no longer purely on revenue growth dynamics, but on whether the segment can sustain margin improvement in an environment of increasing competition and elevated infrastructure spending. At the same time, artificial intelligence is becoming increasingly central, particularly the integration of Gemini models across the Google ecosystem. The key question is whether AI is beginning to generate incremental monetization within existing products or whether it remains primarily a technological layer enhancing user experience without a meaningful impact on revenue structure. In other words, the market is trying to determine whether AI is improving unit economics or simply reshaping product usage patterns.

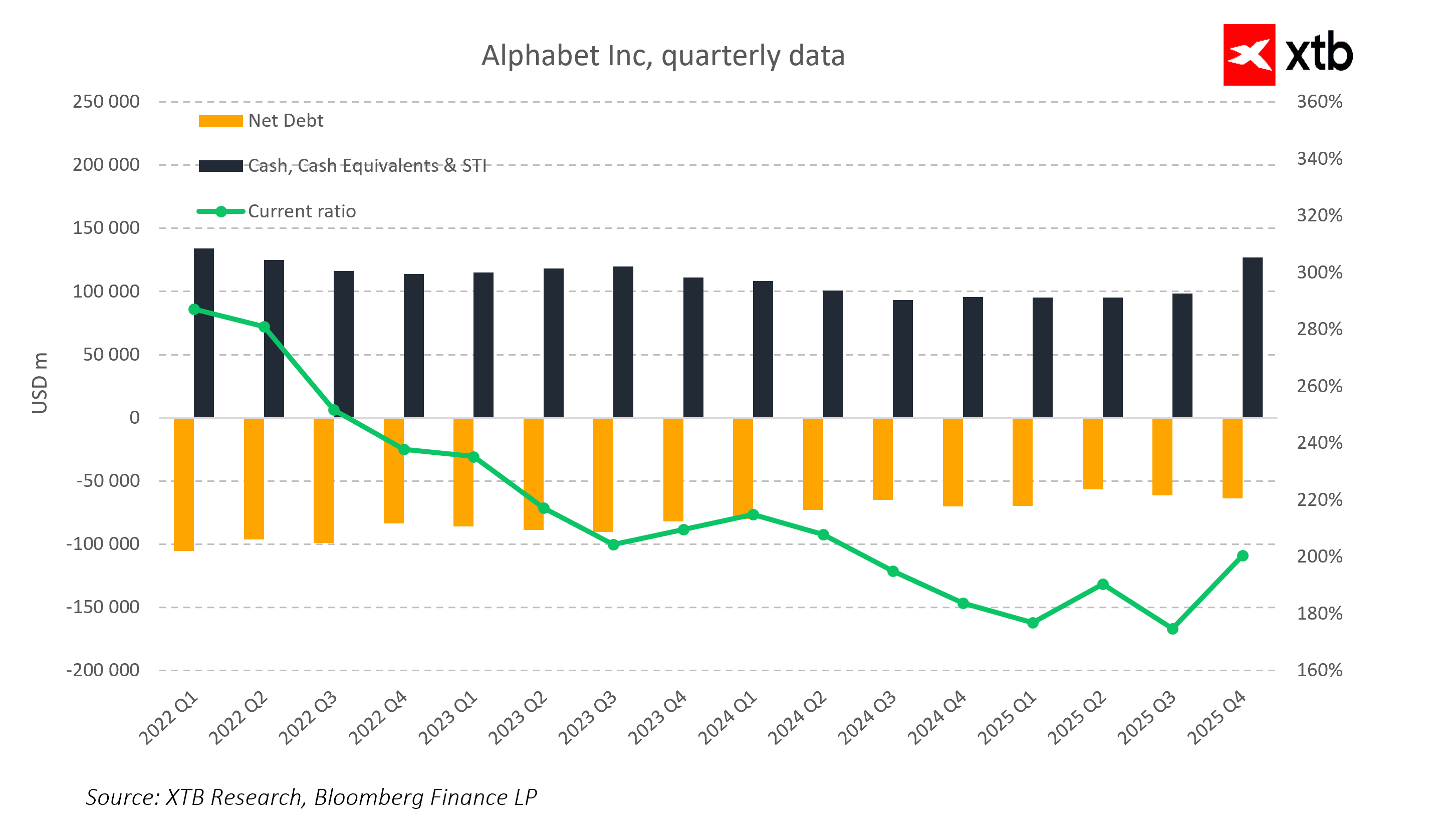

Capital expenditures and pressure on capital efficiency

Alphabet remains in a phase of very aggressive investment expansion, particularly in data centers and computing infrastructure required for AI development. This stage of the cycle naturally elevates CapEx levels and increases investor focus on the relationship between spending and the pace of monetization of new technologies. As a result, financial results will be interpreted not only through the lens of growth dynamics, but also through capital allocation efficiency. The market is increasingly distinguishing between growth driven by genuine operational improvement and growth fueled by rising investment intensity.

Advertising as a stabilizing anchor during transformation The advertising segment remains the core pillar of Alphabet’s business model and the primary source of stable cash flow generation. It continues to finance the ongoing investment cycle while absorbing volatility related to AI and cloud expansion. At the same time, this segment itself is undergoing a structural transformation. The introduction of AI-driven solutions in search and recommendation systems is changing how content is presented and how users interact with advertising. As a result, investors will closely monitor whether this transformation enhances monetization or gradually dilutes it.

High expectations and limited room for disappointment

Current market positioning leaves Alphabet operating in an environment with very limited tolerance for disappointment. The company is priced as one of the leading players in the global AI cycle, which significantly raises the bar for each upcoming earnings release. The most sensitive areas for the market are concentrated around three key factors: Google Cloud growth dynamics, the impact of AI on search economics, and the relationship between rising investment levels and their actual return over time. Even small deviations in these areas may have a meaningful impact on investor sentiment.

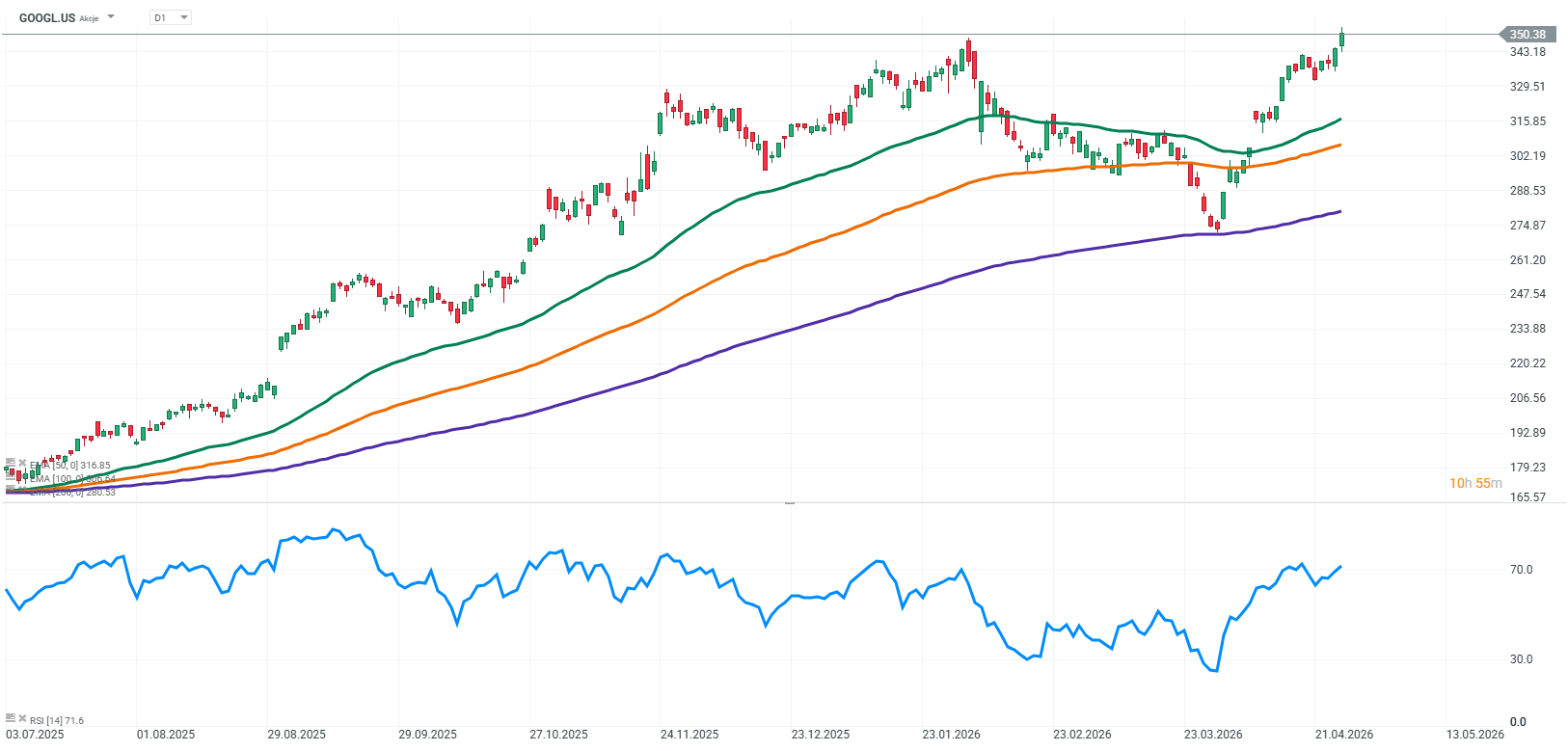

Source: xStation5 Key takeaways

- Alphabet is currently in a phase where the key focus is no longer growth speed, but its quality and durability within an AI-driven model

- Google Cloud and artificial intelligence are becoming the main sources of potential re-rating rather than just additional growth drivers

- The market is increasingly focused on the relationship between CapEx and real AI monetization, treating it as the primary measure of strategic effectiveness

- The advertising segment remains a stabilizing force, but is also undergoing structural transformation driven by AI

- High expectations mean that even solid results may not be enough to trigger a positive reaction if they do not confirm high-quality growth

- The key test for the company is its ability to scale Cloud, AI, and advertising simultaneously without margin erosion or declining capital efficiency