EUR /

EUR /  USD — Euro / US Dollar

USD — Euro / US Dollar JPY — US Dollar / Japanese Yen

JPY — US Dollar / Japanese Yen GBP /

GBP /  AUD /

AUD /  CAD — US Dollar / Canadian Dollar

CAD — US Dollar / Canadian Dollar CHF — US Dollar / Swiss Franc

CHF — US Dollar / Swiss Franc NZD /

NZD / Palantir Earnings – Just below expectations

- May 5, 2026

- Posted by: Today Markets

- Categories: Competitive research, Markets, Technical Analysis

Palantir released its results after Monday’s session ended. The numbers – good enough to put most companies to shame – ultimately came in just slightly below expectations. One of the key efficiency metrics for SaaS companies that Palantir’s management emphasizes is the so‑called “Rule of 40.” In short, it means that the sum of a company’s annual revenue growth rate and its EBITDA margin should be around 40%. For Palantir, this figure stands at roughly 58%, leaving nearly the entire tech sector behind and slightly outperforming Nvidia. Looking at more conventional metrics:

- Revenue: increased to $1.63 billion versus expected ~$1.55 billion.Up 19% q/q and 85% y/y.

- Up 19% q/q and 85% y/y.

- Adjusted EPS: rose to $0.33 versus expectations of ~$0.28.Up 17% q/q and more than 250% y/y.

- Up 17% q/q and more than 250% y/y.

- Adjusted FCF: increased to $924 million.

Guidance for Q2 2026 was set at:

- Revenue: $1.79–$1.80 billion

- Adjusted operating income: $1.063–$1.067 billion

On a full‑year basis, the company raised its outlook:

- Revenue: $7.65 – $7.66 billion

- U.S. commercial revenue: above $3.22 billion

- Adjusted operating income: $4.4 – $4.45 billion

- FCF: $4.2 – $4.4 billion

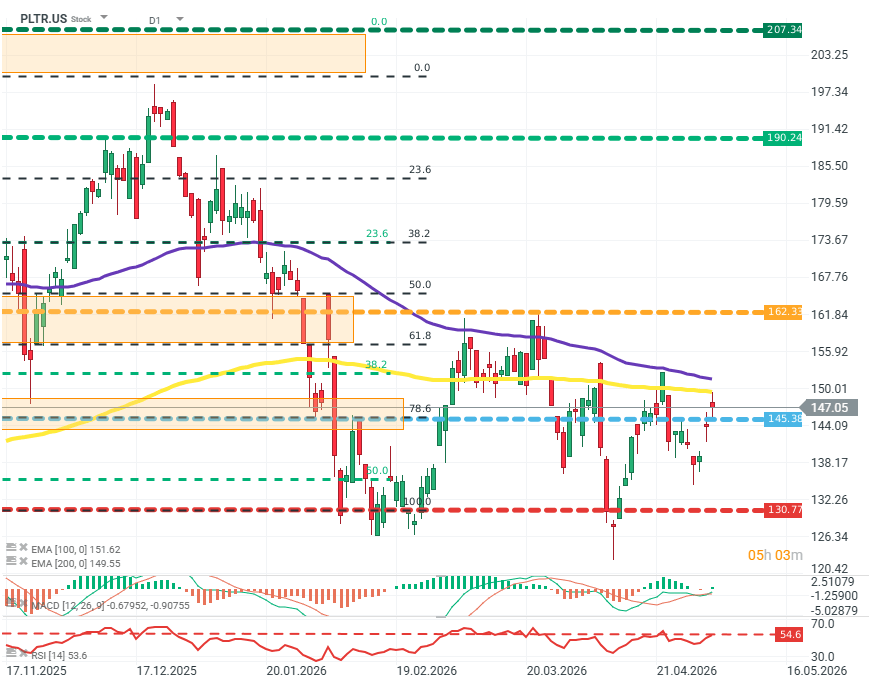

Despite this, the stock reacted with a modest decline of around 3%. So what didn’t land well? Investor concerns focused on revenue in the U.S. commercial segment. Sales grew 133% year over year, but came in below $600 million ($595 million), which was a moderate disappointment for the market. Concerns about the commercial segment are particularly important given the company’s increasing competitive pressure and market penetration by rivals. PLTR.US (D1)

Source: xStation5