Our trading costs

An organized trader should understand what charges or fees they may encounter. A good trading provider ensures that these are presented clearly and transparently, which is what we aim to do.

Here we break down our different costs and fees, plus the reasoning behind them.

Flexible account solutions When you open an account with us, you're in control of your pricing.

|

Account type |

Standard |

RAW Spread account |

|

Description |

For traditional traders, costs to trade is bid/ask spread |

Major FX pairs as low as 0.0 with low commissions |

|

FX spreads |

Variable spreads, EUR/USD as low as 1.0. |

Our tightest spreads, majors as low as 0.0. |

|

Commissions |

Only for equities |

Fixed $5 per $100k USD traded on FX |

|

Volume discounts |

Multi-asset rebates on FX, Indices, Commodities, Metals, cryptocurrencies and Equities, up to $50 per million traded. |

Multi-asset rebates on FX, Indices, Commodities, Metals, cryptocurrencies and Equities, up to $50 per million traded. |

|

Trading platforms |

FOREX.com & MetaTrader |

FOREX.com & MetaTrader |

|

Account applications |

|

|

Rollover Rates

Rollovers are typically the interest charged or earned for holding positions overnight. We strive to keep your trading costs low by sourcing institutional rollover rates and pass them to you at a competitive price. You can earn or pay when a rollover is applied to your position. Rollovers are only applied to open trades at 5pm ET.

Other brokers may calculate rolls continuously, raising your trading costs.

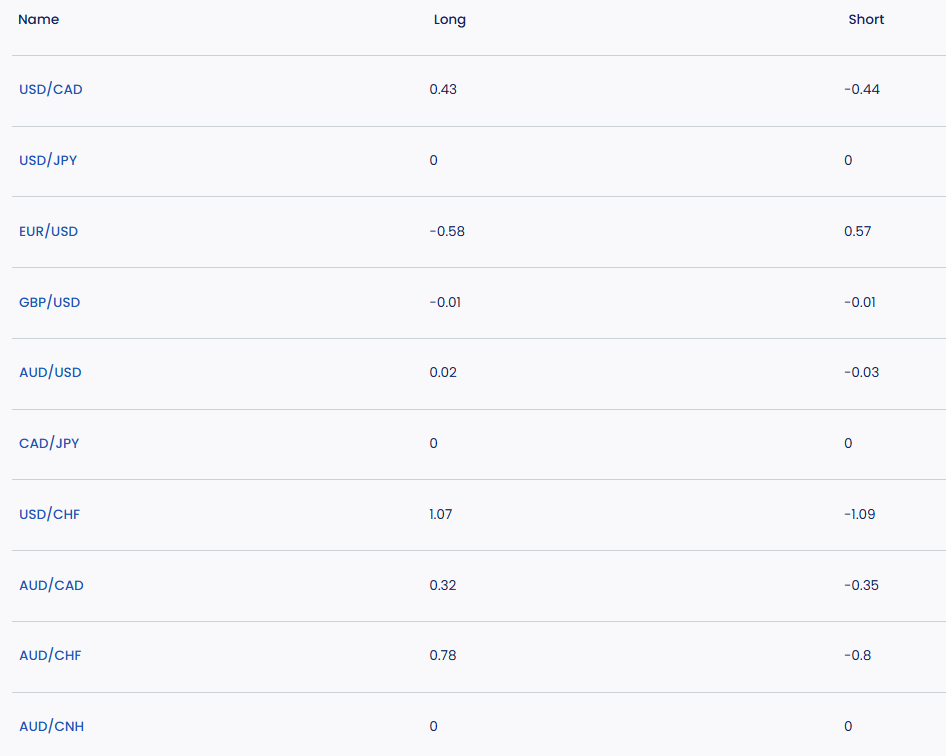

Forex

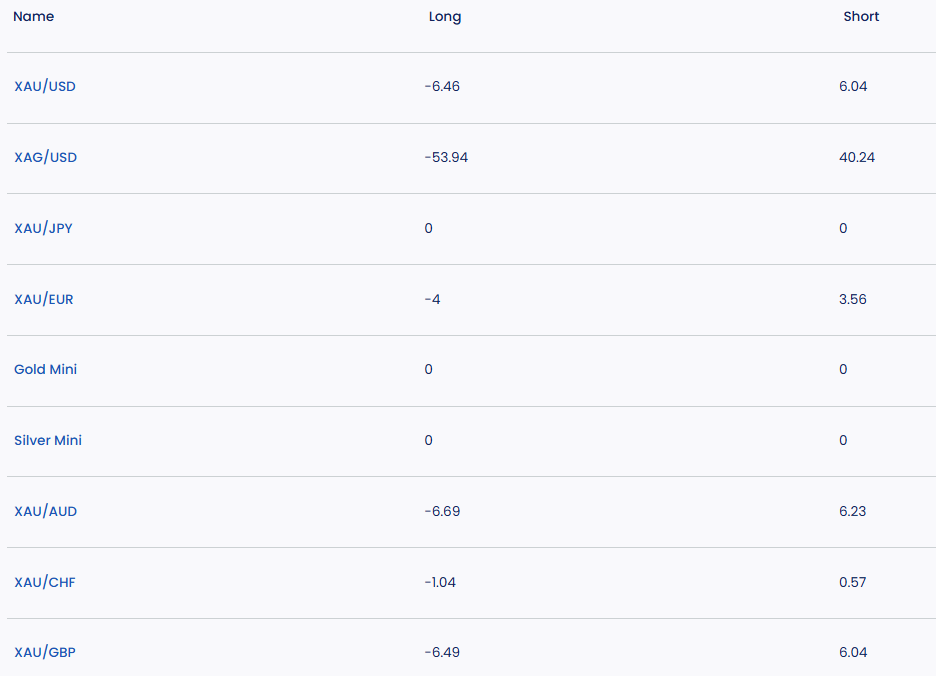

Metals

USD/RUB and EUR/RUB are currently unavailable for trading.

Rollover rates displayed are based on a 10K position and estimated based on the previous rollover rate and number of days being rolled. For example, typically Wednesdays are rolled for three days to account for the weekend. Rollovers also may vary due to month end or holidays.

Direct charges

Spreads

Every market has two prices – the buy and the sell price, the spread is the difference between the buy and sell price.

In the same way a high-street retailer adds a little extra to the price when it buys stock from a wholesaler, the spread is how most trading providers compensate themselves for the service they provide.

Variable spreads

Variable spreads may fluctuate throughout the day. With variable spreads, we will quote you the minimum spread it could be, plus an average spread for a defined historical period of time.

Commission

Stock CFDs are the only asset class where you will have to pay a commission, a one-time fee for opening and closing the trade. Commissions vary by market: for most US stocks it is 1.8 cents per share, and 0.08% of the consideration for most UK, EU, and Asian stocks. Our minimum commission rates are 5 of the stock's base currency. Details on the commission rates for each stock CFD can be found within the Market 360 sheets on the trading platforms.

Potential further adjustments

Rollovers and financing adjustments

When you hold a position overnight, you either pay or receive a rollover fee (also known as a financing charge). These fees fluctuate daily and are different for long and short positions.

Rollovers are only applied to positions that are open at market close in New York – 5pm ET.

A rollover fee is calculated using a swap rate. The swap adjustment is simply the accounting of the cost-of-carry on a day-to-day basis (we do not charge rollover on intraday trades).

The swap rate is measured by the difference in interest rates between the two currencies. We source the swap rate from major financial institutions which base it on a variety of factors such as inflation and key technical indicators.

The rollover rates as calculated as follows:

- Long positions – you are credited/debited by –1 x the trade size x swap points in the unit quote currency

- Short positions – you are debited/credited by the trade size x swap points in the unit quote currency

Example

The swap rates for EUR/USD are 0.817/1.28 and you have a long position of 10,000.

If you held the position overnight, you would be charged a $1.28 rollover fee.

If you had a short position, then you would receive $0.82.

The amounts are then converted back into your base currency.

Financing rates for other markets

How are finance rates calculated?

Financing charges for positions which remain open at our market close are calculated using the following formula:

Short Positions F = V × I / b

Long Positions F = V × I / b, where:

- F = Daily Financing Fee

- V = value of equivalent (quantity x end of day closing price)

- I = applicable Financing Rate

- b = day basis for currency (365 for GBP, HKD and AUD, 360 for all other currencies)

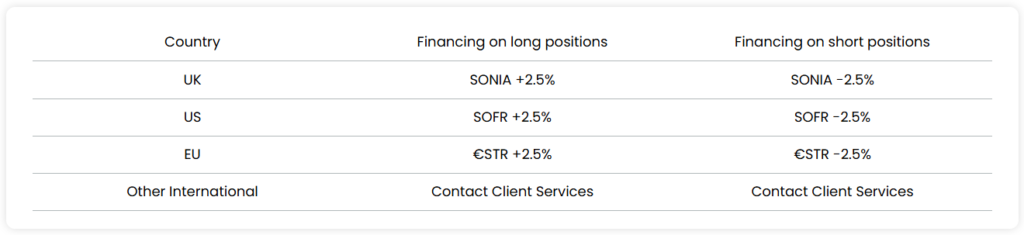

The daily financing fee will be applied to your account each day that you hold an open position (including weekend days). The financing rates are set at benchmark regional interest rate +/- 2.5%.

For example, you are long €10 on the UK 100 and hold the position overnight. UK 100 closes at 6500.

The SONIA rate for that day is 0.33

F = V x I/b

V = 10 (quantity) x 6500 (end of day closing price ) = 65000

I = 0.33 + 2.5% = 2.88%

V x I = 65000 x 2.88% = 1872

F = 1872 / 365 = €5.12 (Daily financing charged, converted into the base currency of your account)

Financing on hedged trades

If you have a hedged position open overnight, you will be charged overnight financing on both sides of the trade.

Dividend Adjustments

When trading our share CFDs, you do not receive any dividends because you do not own the actual stock. Instead, what occurs is a dividend adjustment.

This is because when a company pays out its dividends on the ex-date, the share price takes a slight dip; money has flowed out of the company and into the pockets of the shareholders.

At FOREX.com, we balance the positive effect of the dividend against this dip in the share price.

What happens is that a dividend adjustment occurs at the close of business before the ex-dividend date:

- Long positions are credited

- Short positions are debited

Then all things being equal, the market then opens lower on the ex-date by the dividend amount.

Therefore, the dividend has not impacted your trade or any profit/loss you may have made.

Inactivity fees

A fee of $15 per month is charged to accounts after there is no trading activity for 12 months.

‘Activity’ is defined as placing a trade and/or maintaining an open position during this period. Placing an order on an account without executing a trade will not qualify as activity for these purposes.

If your account has been inactive for a longer period of time, we may need to reassess your trading experience and ensure that we have your up-to-date contact details and information.

You would need to complete our account reactivation form and a member of our Client Services team will be in touch to let you know if we need anything further from you, or to let you know that your account has been reactivated.

Back to base

With CFD trading, the profit or loss will be in the currency of the instrument you trade.

For example, you may have EUR as the base currency for your account, but if you trade Wall Street, the profit or loss for that trade will be in USD. By trading a host of international instruments, you would end up with balances that are comprised of multiple currencies.

FOREX.com has a process called Back to Base, which automatically converts any realized profits or losses, adjustments, fees and charges that are denominated in another currency, back to the base currency of your account.

Borrowing costs

Borrowing costs are incurred when you short a shares CFD position, and reflect a charge incurred in the underlying market when the underlying asset is borrowed in order to sell and return at a later date. Very few markets will incur a borrowing charge, and to determine whether the market you wish to trade has borrowing costs or not, please check the relevant market information sheet or contact us for more details.

Commodity basis adjustment

When trading spot commodity markets, there will be an adjustment to the market price every day. Your account will then be adjusted in the form of a credit or debit to offset the price adjustment.

To price these non-expiring markets, we use two sufficiently liquid futures contracts on the underlying commodity. This is usually the two with the nearest expiry date.

The contract with the closest expiry date is called the ‘front month’ contract and the second-nearest expiry date is called the ‘far month’ contract.

Throughout the duration of the front month contract, the price of the spot commodity market will gradually move from the price of the front month to the price of the far month.

For example, if the front month is market ‘A’ and the far month is market ‘B’ the following would be true.

The market prices move from the price of market ‘A’ towards the price of market ‘B’ as the expiry date of ‘A’ becomes closer. The price of market ‘B’ may be higher or lower, depending on the commodity, than that of market ‘A’.

Daily adjustments for spot commodity markets reflect a day’s movement from ‘A’ towards ‘B’.

For example, if the spot commodity contract is adjusted by +2 points, clients with long positions will be debited 2 x stake and clients with short positions will be credited 2 x stake.

We may use further months should the near, far or both months, become unsuitable to trade.