EUR /

EUR /  USD — Euro / US Dollar

USD — Euro / US Dollar JPY — US Dollar / Japanese Yen

JPY — US Dollar / Japanese Yen GBP /

GBP /  AUD /

AUD /  CAD — US Dollar / Canadian Dollar

CAD — US Dollar / Canadian Dollar CHF — US Dollar / Swiss Franc

CHF — US Dollar / Swiss Franc NZD /

NZD / Microsoft – Is the Giant Already Undervalued?

- April 16, 2026

- Posted by: Today Markets

- Categories: Competitive research, Funding trends, Markets, Technical Analysis

Key takeaways

- Attractive Valuation Metrics: With a forward P/E of 22x (25% below the 5-year average) and a PEG ratio near 1.0x, the stock currently appears significantly undervalued.

- Strong Fundamentals & AI Demand: A record order backlog (RPO) of $625 billion and surging adoption of Copilot and Azure confirm Microsoft’s continued dominance in the tech sector.

- Hardware Self-Sufficiency: The rollout of proprietary Maia and Cobalt 200 chips aims to reduce operational costs and decrease reliance on external providers like Nvidia.

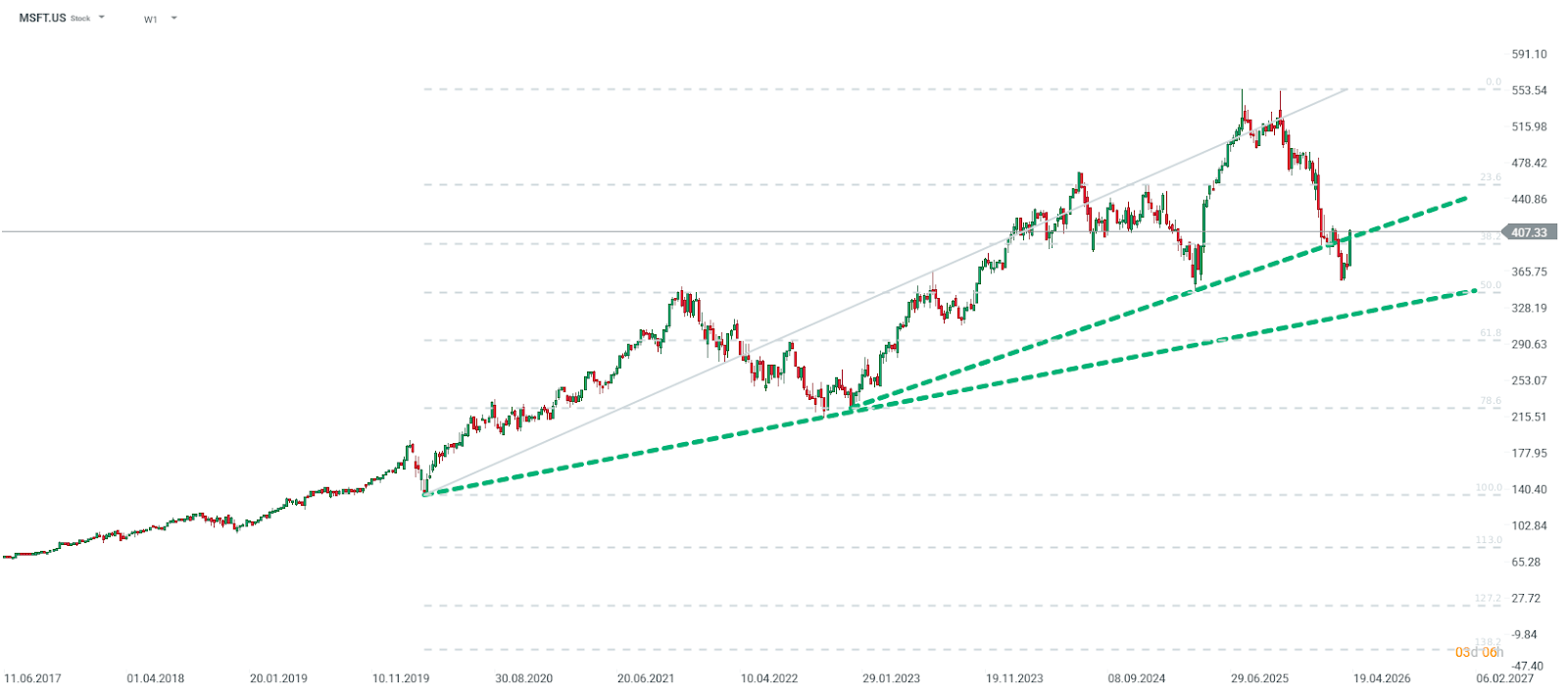

After a period of intense growth driven by enthusiasm for Artificial Intelligence, Microsoft’s (MSFT) shares have entered a correction phase. Although the company recorded a decline of over ⅓ from its historical peaks (from daily highs of $550 in October 2025 to approximately $356 at the end of March 2026), its business fundamentals remain exceptionally solid. Since the recent local bottom, the company has already managed to rise by nearly 15%.

MSFT’s declines halted before the 50% retracement of the upward wave that began after the March 2020 sell-off. Source: xStation5 Attractive Valuations and Ratios The market currently seems to be punishing Microsoft for high capital expenditures (CapEx), while ignoring the increasing efficiency of the business. Wall Street commentators point to very attractive valuation ratios compared to historical averages:

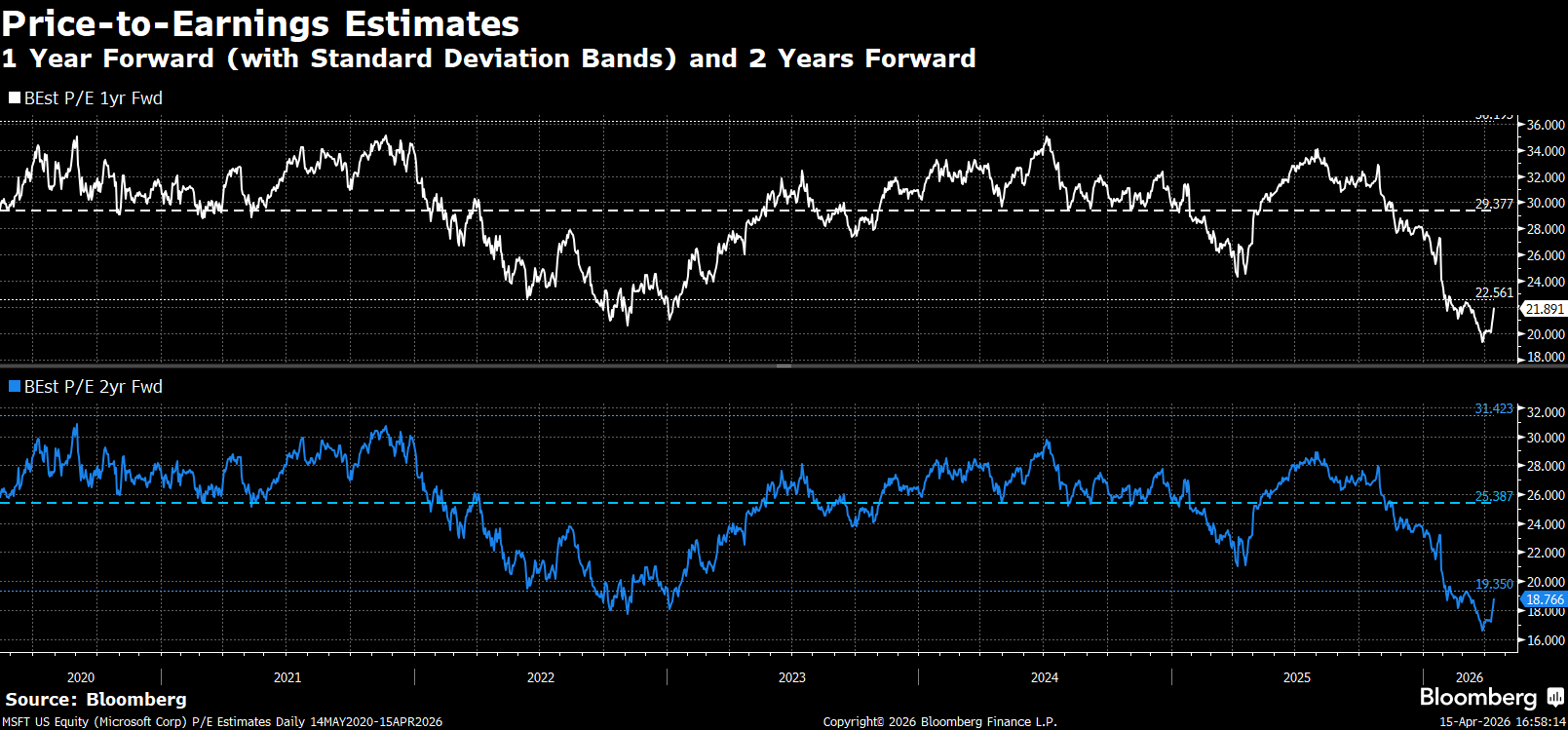

- P/E Ratio (Price/Earnings): Microsoft is currently valued at approximately 22x forward earnings , representing a 25% discount to the 5-year average of nearly 30x. Furthermore, the price relative to 2-year projected earnings is even lower, below 20x—falling below 2022 valuations and more than one standard deviation below the mean.

- PEG Ratio: With earnings growth projected at 23% annually, the PEG ratio is near 1.0x , making the company attractive for GARP (Growth at a Reasonable Price) investors.

- Cash Reserves: The cash-generating capability of Microsoft’s assets reached a record level of 26.6% , proving the high quality of management under Satya Nadella. In an era where cash is not necessarily visible in companies spending massive amounts and reporting only future potential profits, cash remains one of the key aspects of long-term valuation.

Microsoft is already very attractive looking at the forward P/E ratio. Source: Bloomberg Finance LP

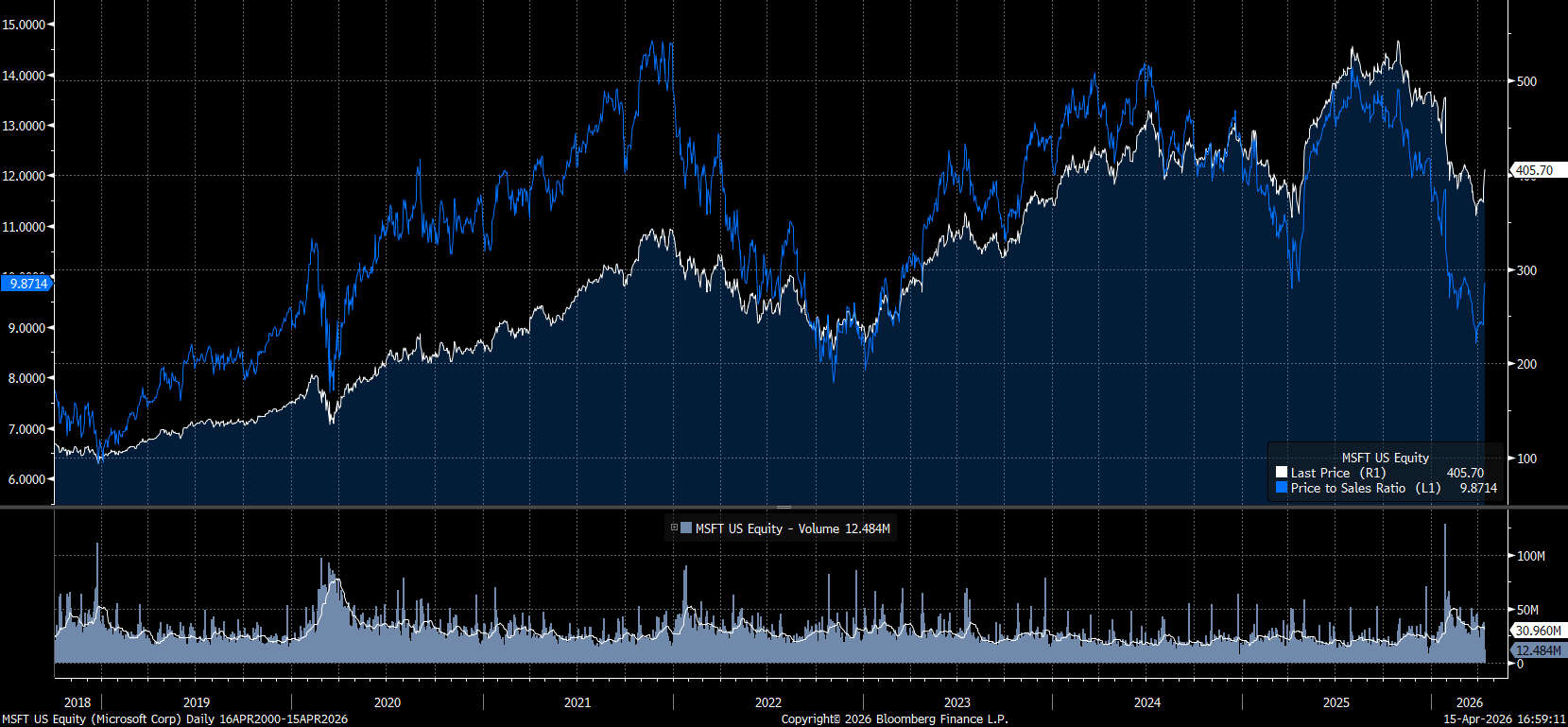

The P/S ratio has dropped to levels near 2020 and 2022, which may indicate attractive valuations even with the price significantly higher than back then ($150 and $200 per share). Source: Bloomberg Finance LP Pillars of Future Growth Despite investor concerns regarding AI competition, market data suggests that Microsoft’s position is secure:

- Copilot Adoption: Nearly half of the large companies surveyed have already deployed Copilot into operation, and Microsoft leads in solutions for securing AI workloads.

- Azure Dominance: As many as 85% of respondents plan to increase spending on Azure cloud services, the highest result in five quarters.

- Hardware Independence: The introduction of proprietary chips ( Maia 200, Cobalt 200 ) aims to lower operating costs and reduce dependence on external providers such as Nvidia.

Outlook and Risks A key point for investors will be the upcoming third-quarter fiscal results (release on April 29, 2026). The market expects confirmation that massive infrastructure investments (CapEx at $37.5 billion per quarter ) are translating into real orders. The commercial Remaining Performance Obligation (RPO) currently stands at a record $625 billion , providing a solid foundation for future revenue. The primary risks remain the concentration around OpenAI and potential pressure on FCF margins in the short term. Nevertheless, at current price levels and technical support near $340–$375, Microsoft appears to be a company with a favorable risk-reward profile, offering exposure to cutting-edge technologies at an increasingly reasonable valuation. If the situation in the Middle East improves, capital will likely begin to flow back into the market in a broad stream, which could also positively impact companies that have been heavily oversold in recent months, including Microsoft.