EUR /

EUR /  USD — Euro / US Dollar

USD — Euro / US Dollar JPY — US Dollar / Japanese Yen

JPY — US Dollar / Japanese Yen GBP /

GBP /  AUD /

AUD /  CAD — US Dollar / Canadian Dollar

CAD — US Dollar / Canadian Dollar CHF — US Dollar / Swiss Franc

CHF — US Dollar / Swiss Franc NZD /

NZD / Will US drought fuel speculative grain volatility on CBOT?

- April 25, 2026

- Posted by: Today Markets

- Categories: Blog, Funding trends, Markets, Soft Commodities, Technical Analysis

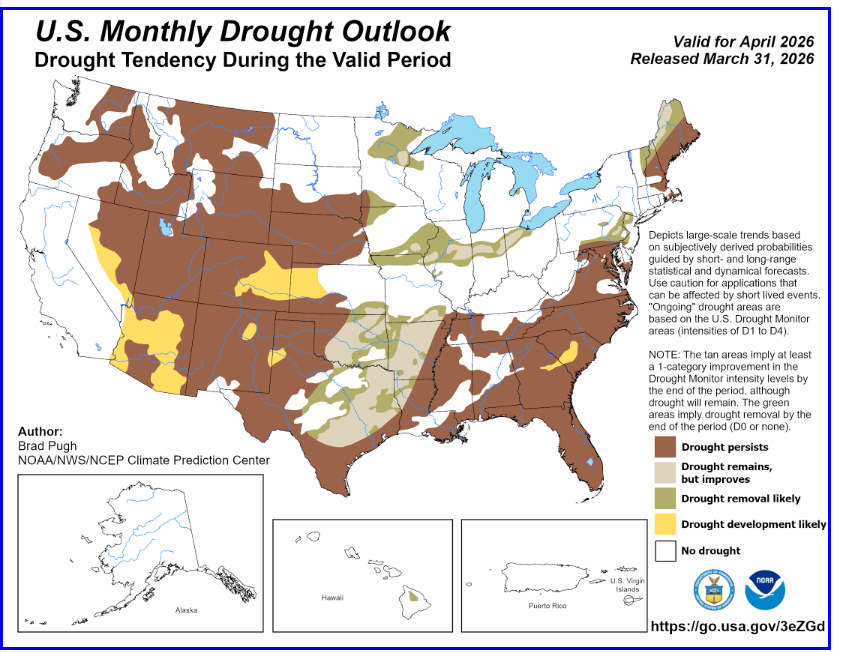

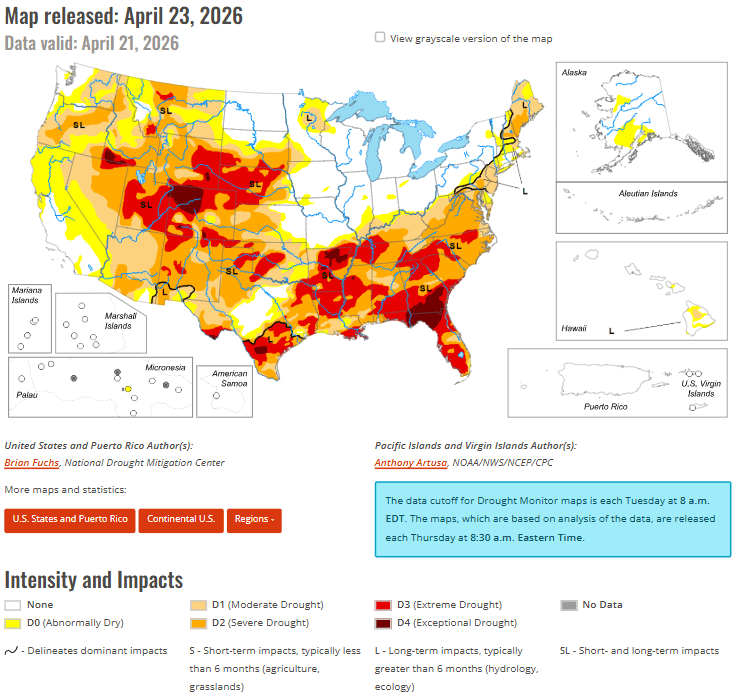

Futures on wheat, corn, and soybeans traded on the Chicago Board of Trade (CBOT) have moved higher in recent weeks. According to NOAA weather reports, significantly above-average temperatures and below-average precipitation in March led to the expansion and intensification of drought conditions across the western United States and the Great Plains. Drought is expected to persist across the western regions through April, with further development most likely in parts of Arizona and Nevada.

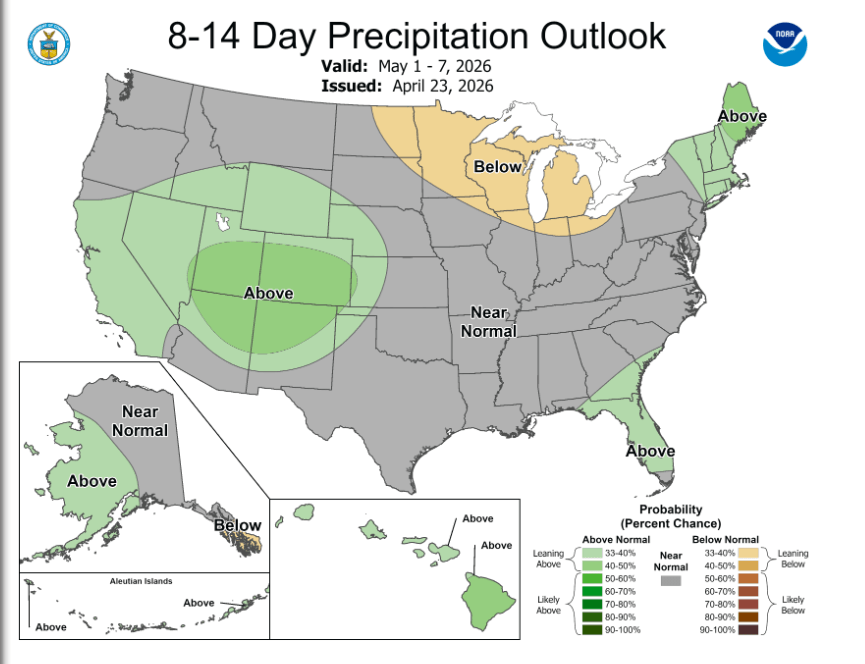

- A wet start to the month may delay widespread drought development in the Pacific Northwest, the Northern Intermountain West, and northern California. However, drought expansion is still expected in these regions later in the spring.

- Drought development is forecast for eastern Colorado, western Kansas, northeastern New Mexico, and the Texas Panhandle.

- In contrast, improvement or easing of drought conditions is more likely in eastern Oklahoma, central to northeastern Texas, northwestern Louisiana, the Ozarks region, and the Midwest

- In the southeastern United States, drought is expected to persist and potentially intensify, while in parts of the Northeast, conditions are more likely to improve or be fully alleviated.

Source: NOAA

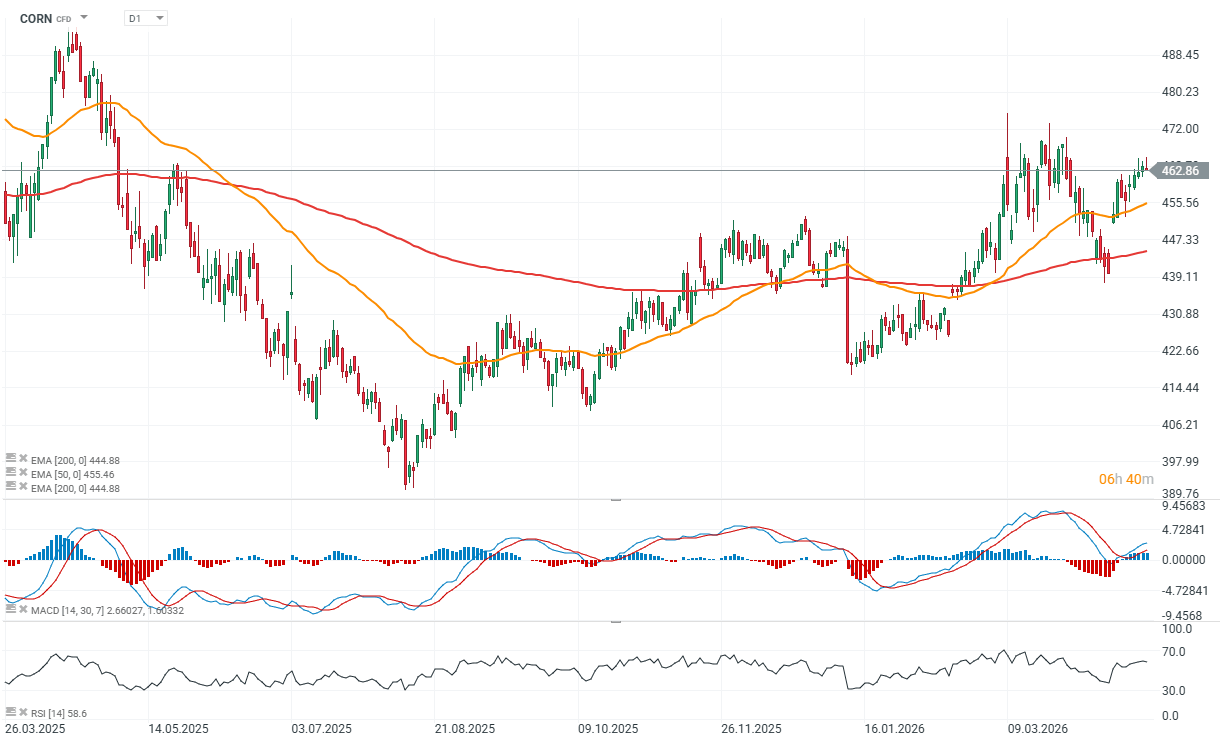

Short-term market fundamentals (corn) – practitioner’s view

The corn market is starting the session on a stable footing after pulling back from recent highs. Importantly, the short-term structure remains constructive, with prices forming higher lows across most recent sessions, suggesting underlying demand is still present, albeit without strong momentum. The past two weeks have brought gradual but consistent gains, supporting the bullish case. Key drivers include concerns over soil moisture in the U.S. Midwest and the potential for reduced acreage, alongside solid export demand, which continues to cushion downside moves.

That said, the weather outlook remains mixed. Conditions have improved in parts of the central and eastern Corn Belt, but western regions and the southeastern U.S. remain dry. The share of corn affected by drought has risen to 27% (vs. 26% a year ago), which is beginning to matter for the market. Rainfall is expected across the Plains and Midwest in the coming days, potentially improving crop conditions in the short term, although cooler temperatures may slow fieldwork. In South America, the picture is also mixed—harvests in Argentina are progressing, while Brazil faces hot and dry conditions in key safrinha regions, which could impact supply in the weeks ahead. Globally, the International Grains Council has cut its corn production forecast by 3 million tonnes to 1.3 billion tonnes, signaling emerging cost pressures in the agricultural sector.

Exports – solid, but need to accelerate

Export data remains decent, though not strong enough to shift sentiment decisively. For the week ending April 16:

- 1.316 million tonnes were sold for the current marketing year

- 440,000 tonnes for the next marketing year

This brings total sales to 1.76 million tonnes. Cumulative exports have reached 88.4% of the USDA forecast, slightly above the 5-year average of 87.3%. However, weekly sales need to average around 496,000 tonnes to meet the annual target.

Key levels and baseline scenario

From a trading perspective, the structure remains relatively clear:

- support for July contract: around 450

- support for December contract: 478 , with a secondary level at 456

- resistance for July contract: 468–472

The market appears to be stabilizing with a slight bullish bias, but lacks a strong catalyst for a breakout. Pullbacks are likely to find support in fundamentals, particularly export demand and weather uncertainty. In short: fundamentals are not decisively bullish, but strong enough to limit deeper declines. The market remains in a “waiting for a catalyst” phase.

Source: xStation5

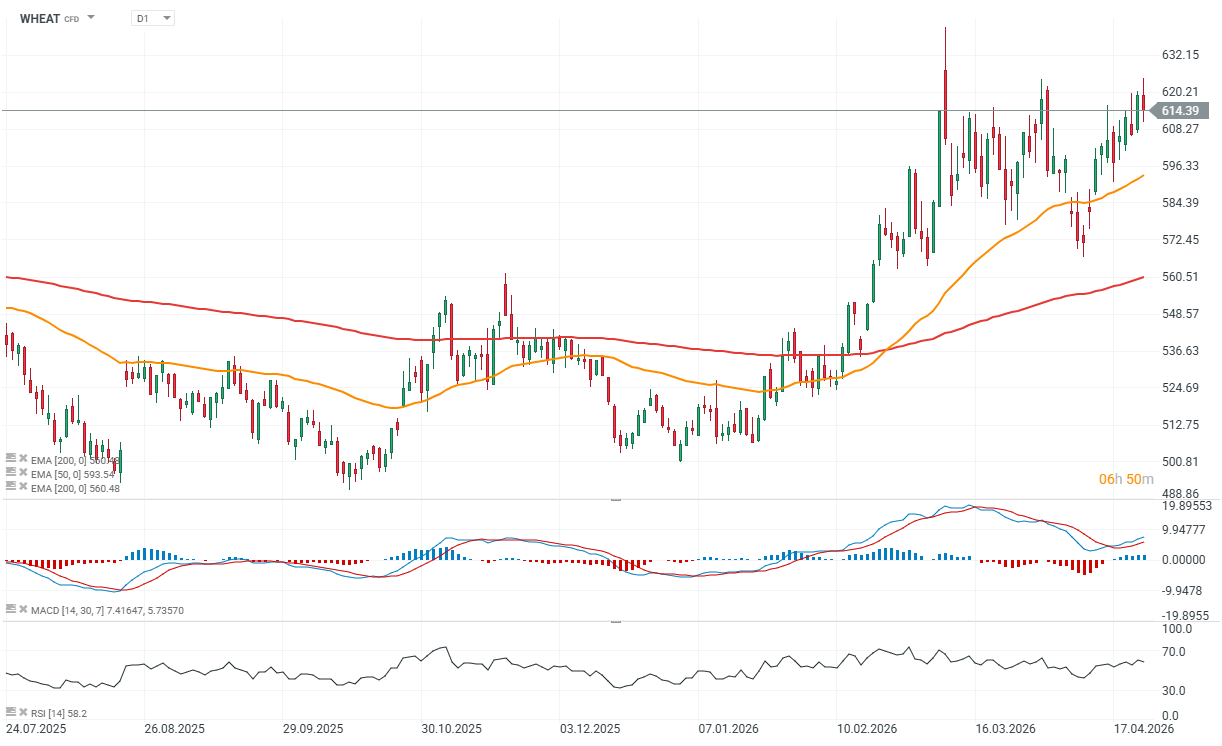

Short-term market fundamentals (wheat) – practical view

Wheat is pulling back after sharp gains, particularly in Kansas contracts. This looks more like a correction than a trend reversal, as updated weather models show rainfall across much of the Plains (excluding the far Southwest), temporarily easing the weather premium. However, crop damage has likely already occurred, and even improved conditions may not significantly restore yields. As such, the current pullback appears technical rather than fundamentally driven.

Global fundamentals – tight supply remains key

The main supportive factor remains unchanged: weaker global production prospects. Lower planted acreage is expected not only in the U.S., but also in Ukraine, Argentina, Australia, France, and Zimbabwe. The International Grains Council has reduced its global production forecast by another 1 million tonnes to 821 million tonnes, and further downward revisions are possible. This keeps supply tight and supports prices in the medium term.

Geopolitics and costs – underlying support

Geopolitical tensions continue to play a role. Ongoing disruptions and risks to trade routes suggest that energy and fertilizer costs are unlikely to decline meaningfully in the near term. This directly impacts production costs and limits supply expansion, effectively acting as a floor for prices.

Export demand – steady but not aggressive

Export activity remains moderate. For the week ending April 16:

- 129,000 tonnes were sold for the current season

- 8,000 tonnes for the next season

Totaling 137,000 tonnes, cumulative sales have reached 100.1% of the USDA forecast (vs. 92.8% 5-year average), meaning export targets have effectively already been met. There are also reports of U.S. buyers sourcing Polish milling wheat due to relatively high domestic prices, indicating active global trade flows.

Correction within an uptrend

In market terms, this is a classic scenario: a short-term pullback driven by improved weather forecasts, while underlying fundamentals remain supportive. The market continues to price in weather risk, and any deterioration in conditions or further supply cuts could quickly reignite upward pressure.

Source: xStation5

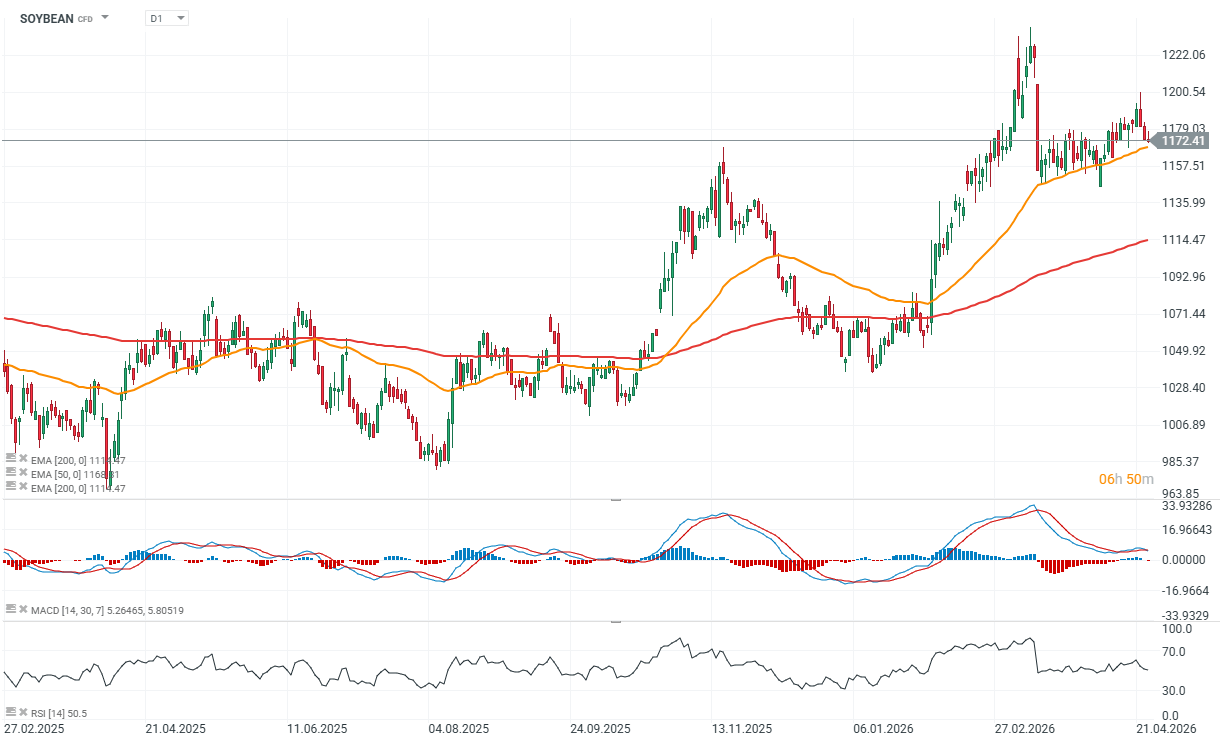

Short-term market fundamentals (soybeans) – practical view

The soybean market continues to weaken following Wednesday’s reversal, with the short-term technical picture deteriorating. Bullish momentum has faded, as earlier supportive factors—such as potential acreage declines, drought concerns, and the end of the Brazilian harvest—are no longer sufficient. Argentina’s harvest is progressing, and U.S. weather conditions are generally better than a year ago, with a larger share of drought-free areas. Forecasted rainfall across the Midwest and Plains may slow fieldwork but improve crop conditions, reducing perceived risk.

Fund positioning and technical pressure

Recent declines were driven primarily by long liquidation, especially in beans and meal. Funds still hold significant long positions across the soybean complex, but the failure to break higher and the rejection of resistance have shifted the balance toward the bears. Technically, the market looks weaker, with fading momentum and no clear support emerging. In the near term, capital flows and positioning matter more than fundamentals.

Exports – no clear catalyst Export data remains mixed:

- Soybeans : 364,000 tonnes sold + 5,000 tonnes for next season (91.9% of USDA forecast vs. 93.9% 5-year average; needs ~173,000 tonnes weekly)

- Soybean meal : 162,000 tonnes sold (with slight downward revisions) (79.9% vs. 74.6% average; needs ~148,000 tonnes weekly)

- Soybean oil : minimal sales (1,500 tonnes) (67.4% vs. 69.7% average; needs ~7,400 tonnes weekly)

Overall, there is still no strong demand signal to shift sentiment. Market outlook: downside risk building Technically, the market is weakening, with July contracts potentially testing the lower boundary around 1160 . A break below this level could trigger a deeper sell-off, particularly if funds accelerate long liquidation. Declining open interest suggests this process may already be underway. That said, weather remains a key wildcard—any renewed deterioration could quickly shift sentiment back in favor of the bulls.

Source: xStation5

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.