EUR /

EUR /  USD — Euro / US Dollar

USD — Euro / US Dollar JPY — US Dollar / Japanese Yen

JPY — US Dollar / Japanese Yen GBP /

GBP /  AUD /

AUD /  CAD — US Dollar / Canadian Dollar

CAD — US Dollar / Canadian Dollar CHF — US Dollar / Swiss Franc

CHF — US Dollar / Swiss Franc NZD /

NZD / Cocoa prices are rising again. Will chocolate become even more expensive?

- July 1, 2026

- Posted by: Today Markets

- Categories: Competitive research, Markets, Soft Commodities, Technical Analysis

Key takeaways

- ICE cocoa futures have climbed back above $5,000 per tonne, nearly doubling from their late-February lows as investors once again price in weather risks across West Africa.

- The growing likelihood of a strong El Niño event, combined with early signs of weaker crop development in Ivory Coast, has renewed concerns about cocoa supplies for the 2026/27 season, despite still-elevated global inventories.

- The coming weeks could prove decisive for the cocoa market, as July field surveys will determine whether the recent price rebound is supported by deteriorating crop conditions or whether investors will shift their focus back to abundant inventories and subdued demand.

Just four months ago, it seemed that the most explosive phase of the cocoa rally had finally come to an end. After retreating sharply from record highs, ICE cocoa futures steadily lost ground as investors increasingly focused on the return of a global supply surplus. That narrative is becoming less convincing once again. Cocoa prices have climbed back above $5,000 per tonne , nearly doubling from the lows recorded at the end of February. The market is once again pricing in weather risks across West Africa, the region responsible for the majority of global cocoa production. The key question now is whether this rebound is simply a correction after an excessive selloff or the beginning of a broader bullish trend.

Weather is back in the driver’s seat Weather risks in West Africa have once again become the dominant force shaping cocoa prices, with investors increasingly concerned about the impact of El Niño on the upcoming harvest.

The biggest catalyst in recent days has been the return of El Niño concerns. Japan’s Meteorological Agency officially confirmed the development of the weather pattern across the Pacific, while the U.S. National Oceanic and Atmospheric Administration estimates a roughly 67% probability of a very strong “Super El Niño.” For the cocoa market, this matters enormously. El Niño typically brings hotter and drier conditions to West Africa, reducing soil moisture during one of the most important stages of cocoa tree development. Cocoa is particularly vulnerable to prolonged dry weather, which can weaken trees, reduce pod formation and ultimately lower yields. This is why traders react well before any production losses are officially confirmed. On the cocoa market, expectations often move prices long before harvest data becomes available. Growing concerns that the main crop beginning in September could disappoint have already become a meaningful support for futures.

Early crop surveys raise fresh concerns Initial assessments of the 2026/27 crop point to weaker pod development, increasing concerns that the next main harvest may fall well short of last year’s levels.

Weather forecasts are not the only reason behind the recent rally. Early field surveys in Ivory Coast indicate below-average formation of young cocoa pods, known as cherelles, providing one of the first warning signs for the upcoming season. Preliminary estimates suggest Ivory Coast could produce around 1.8 million tonnes during the harvest beginning in September, compared with approximately 2.2 million tonnes expected for the current season. That gap is substantial and helps explain why cocoa futures have rebounded so aggressively from their February lows. The market is now waiting for updated field surveys in July, which should provide a much clearer picture of the production outlook. If those reports confirm weak pod development, cocoa prices could remain well supported.

Supply growth is still limiting optimism Despite the recent rally, current supply data still point to relatively comfortable market conditions, preventing investors from fully embracing a new bullish cycle.

Only a few weeks ago, cocoa prices were under pressure because of signs that global supplies were improving. Ivory Coast reported that more than 2.04 million tonnes of cocoa had arrived at its ports since the beginning of the marketing season, roughly 20% higher than a year earlier. Nigeria also reported a 28% year-over-year increase in cocoa exports during May. At the same time, ICE-certified cocoa inventories have climbed to their highest level in almost two years, exceeding 2.94 million bags . Historically, rising inventories tend to cap further price gains. For that reason, the current rally appears to reflect concerns about future production risks rather than an immediate shortage of physical cocoa.

Cocoa demand remains under pressure Demand continues to soften across key consuming regions as chocolate manufacturers struggle with the consequences of exceptionally high cocoa prices.

Demand remains one of the weakest parts of the current market picture. In North America, first-quarter cocoa grindings declined 3.8% year-over-year . Europe performed even worse, with grindings falling 7.8% , marking the weakest first quarter in 17 years . For chocolate manufacturers, elevated cocoa prices translate directly into higher production costs and pressure on margins. Many companies have reduced purchases, delayed orders, or adjusted product formulations to reduce cocoa content where possible. Asia remains the exception. Cocoa processing there increased by more than 5% , although much of the increase is believed to reflect inventory rebuilding rather than a broad-based recovery in consumer demand.

Farmers are not always benefiting from higher futures prices Lower farmgate prices in Ghana and Ivory Coast could discourage long-term investment in cocoa plantations, despite the recent recovery in international futures prices.

The cocoa market has an unusual characteristic: rising futures prices do not necessarily translate into higher incomes for farmers. Ghana reduced the official farmgate price paid to cocoa growers by nearly 30% for the 2025/26 season, while Ivory Coast also introduced significant cuts for its mid-crop harvest. This matters because the two countries account for well over half of global cocoa production. Lower farm incomes reduce incentives to invest in fertilizers, crop protection and plantation renewal, potentially affecting future output. Cameroon presents a different picture. Farmgate cocoa prices have climbed to their highest level of the current marketing season, reaching 2,100–2,250 CFA francs per kilogram . Even so, they remain well below the exceptional highs recorded during the previous two seasons.

Surplus forecasts are becoming more conservative Analysts still expect a global cocoa surplus, but projections have been revised sharply lower as weather risks continue to increase.

StoneX recently reduced its forecast for the global cocoa surplus in the 2026/27 season from 267,000 tonnes to 149,000 tonnes , largely because of growing concerns that El Niño could damage West African production. The firm’s surplus forecast for the current 2025/26 season was also lowered, from 287,000 tonnes to 247,000 tonnes . The market is therefore not pricing in a global deficit yet. However, the expected supply cushion has become noticeably smaller, making prices increasingly sensitive to any deterioration in weather conditions. Investors remember how quickly supply concerns pushed cocoa prices to record highs over the past two years, making them far less willing to ignore early warning signs.

What comes next for cocoa prices? The next few weeks could prove decisive, as July crop surveys may determine whether the current rally has solid fundamental support or is simply another short-term rebound.

The cocoa market currently faces a complicated balance of bullish and bearish forces. On one hand, inventories remain elevated, Ivory Coast’s port arrivals continue to show healthy supply, and demand across Europe and North America remains weak. On the other hand, traders are increasingly focused on the 2026/27 crop, where weather risks continue to grow. If El Niño brings significantly drier conditions to West Africa and upcoming surveys confirm weak pod development, cocoa could remain one of the strongest-performing commodities during the second half of the year. If weather conditions prove more favorable, attention may quickly shift back toward abundant inventories and sluggish demand. For now, cocoa futures have reclaimed the $5,000 per tonne level after nearly doubling from their February lows. The speed of that recovery illustrates just how sensitive this market remains to weather forecasts and changing expectations for future supply.

Will chocolate prices rise again? The market is sending mixed signals Although cocoa prices are rebounding sharply, weak chocolate demand and improving supply conditions suggest another wave of retail price increases is far from inevitable.

Global chocolate demand continues to feel the effects of record-high cocoa prices seen over the past two years. First-quarter 2026 grinding data reveal significant regional divergence. European cocoa grindings declined 7.8% year-over-year to 325,900 tonnes , the weakest first-quarter performance in 17 years. North American grindings fell 3.8% to 106,100 tonnes , while Brazilian processing slipped 0.8% to 51,700 tonnes . Asia was the clear exception, with grindings rising 5.2% year-over-year to 223,500 tonnes , representing a remarkable 13.4% increase compared with the previous quarter. Barry Callebaut, the world’s largest chocolate manufacturer, acknowledges that years of exceptionally high cocoa prices have significantly weakened consumer demand.

The company has reported declining sales volumes and weaker profitability, prompting a greater focus on higher-margin business segments. Analysts also caution that Asia’s stronger grinding activity should not necessarily be interpreted as a full recovery in chocolate consumption, as much of the increase appears to reflect inventory rebuilding of cocoa butter and cocoa powder. Meanwhile, supply conditions have gradually improved. Cocoa arrivals at Ivory Coast’s ports are running nearly 19% higher than a year ago, while ICE-certified inventories have reached their highest level in almost two years. As a result, if El Niño fails to significantly damage the 2026/27 harvest, chocolate manufacturers could benefit from more stable cocoa prices over the coming quarters, making another broad wave of retail price increases relatively unlikely.

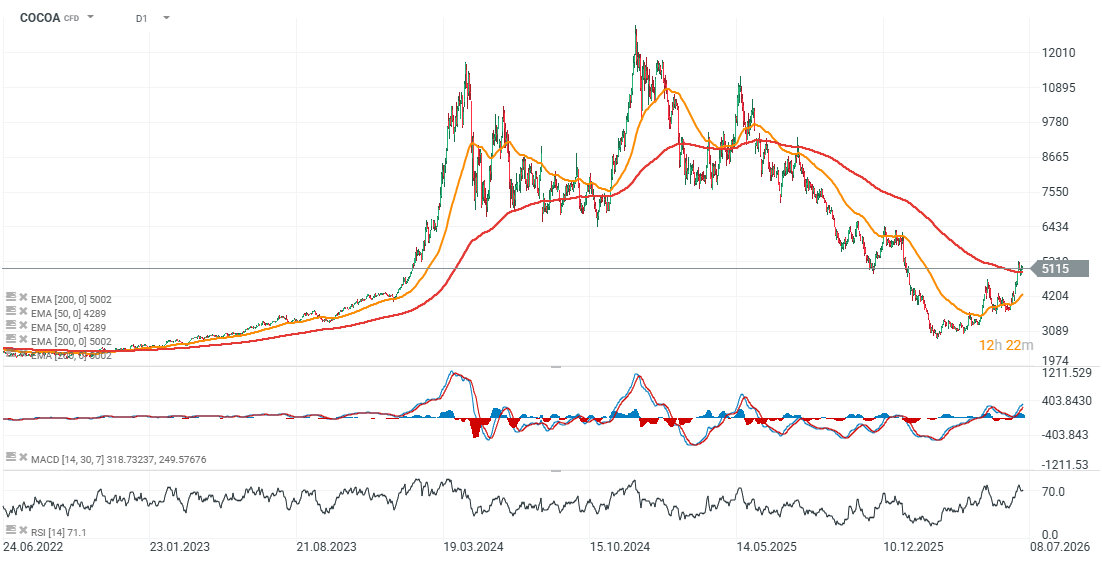

Cocoa technical outlook (Daily chart) Cocoa futures have broken back above the 200-day exponential moving average (EMA200), signaling an attempt to reverse the recent downtrend and resume a broader upward move.

Source: xStation 5