EUR /

EUR /  USD — Euro / US Dollar

USD — Euro / US Dollar JPY — US Dollar / Japanese Yen

JPY — US Dollar / Japanese Yen GBP /

GBP /  AUD /

AUD /  CAD — US Dollar / Canadian Dollar

CAD — US Dollar / Canadian Dollar CHF — US Dollar / Swiss Franc

CHF — US Dollar / Swiss Franc NZD /

NZD / Trade of The Day – WHEAT

- June 3, 2026

- Posted by: Today Markets

- Categories: Markets, Soft Commodities, Technical Analysis

Facts

- As of 8:52 AM GMT, the CBOT Chicago WHEAT contract is trading near 597 and continues to move lower.

- The CME Group May AgBarometer showed a slight deterioration in farmer sentiment. The index fell to 119 points from 121 in April.

- The Current Conditions Index declined by 8 points, reaching its lowest level since December 2024.

- Meanwhile, the Future Expectations Index rose by 1 point, signaling slightly greater optimism regarding the sector’s outlook.

- Favorable weather conditions across the U.S. Wheat Belt are improving yield expectations.

- Ukraine’s grain traders association UGA forecasts grain and oilseed production to rise to 83.6 million tonnes in 2026, compared with 80 million tonnes a year earlier. The country’s exportable surplus could increase to 50.8 million tonnes.

- The USDA estimated global wheat ending stocks for both the 2025/26 and 2026/27 marketing years at 3.7 million tonnes and 5.5 million tonnes, respectively, below average market expectations. For 2026/27, global wheat ending stocks are projected at 275 million tonnes, down 4.2 million tonnes from the previous season.

- The USDA forecasts that U.S. wheat production in the 2026/27 season could fall to its lowest level in more than 50 years due to reduced planted acreage and persistent drought across the Great Plains.

- At the same time, analysts at the Agricultural and Horticulture Development Board (AHDB) note that global wheat ending stocks remain 1.3% above the five-year average, which could limit the potential for stronger price gains unless weather-related risks intensify further.

- In its latest World Agricultural Supply and Demand Estimates (WASDE) report, the USDA projects a decline in global wheat production, partly due to the significant deterioration in U.S. production prospects.

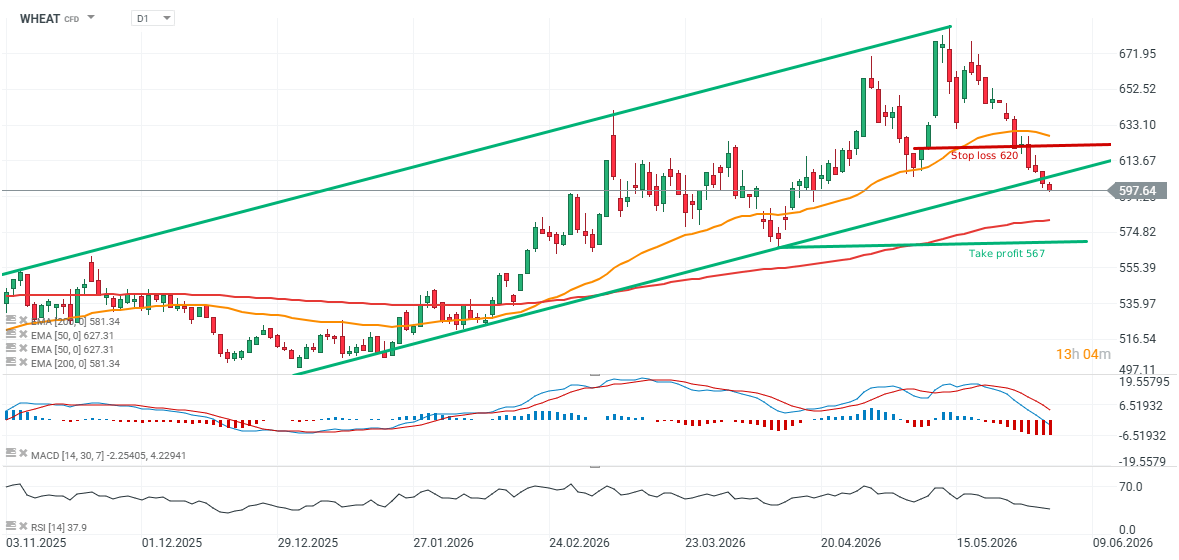

Recommendation Short position on WHEAT at market price

- Stop Loss: 620

- Take Profit: 567

Opinion

CBOT wheat futures ended lower as the U.S. harvest gets underway and demand remains weak. The start of the Northern Hemisphere harvest season is increasing short-term supply and adding downward pressure on prices. Supply-side factors currently dominate the market and continue to weigh on futures prices. Despite temporary support from higher oil prices, investors quickly returned their focus to fundamentals, where expectations of abundant harvests across multiple producing regions remain the key driver. Particularly important are expectations surrounding the upcoming Northern Hemisphere harvests, which will bring fresh grain supplies to the market and traditionally encourage producers to increase forward-selling activity. This year, the USDA projects U.S. wheat production at 1.56 billion bushels, down 21% year-over-year and the lowest level since 1972.

However, the United States accounts for only around 6-7% of global wheat production, meaning weak U.S. harvests do not necessarily imply a global shortage. Meanwhile, Russia remains the world’s largest wheat exporter and continues to offer wheat at competitive prices. Although the strong ruble has reduced pressure on Russian exporters, Russian wheat remains competitive relative to U.S. grain in key import markets. Favorable weather conditions have improved prospects for parts of the current crop, although the market believes much of the damage caused by earlier drought conditions is irreversible, leaving production forecasts among the weakest seen in decades. An additional headwind remains weak demand for U.S. wheat. The limited competitiveness of U.S. exports continues to hinder improvements in the supply-demand balance and reduces the potential for a sustained recovery in CBOT wheat prices. Selling pressure has also intensified as U.S. winter wheat harvesting begins, prompting farmers to increase hedging activity in the futures market.

Declines in corn and soybean prices have also negatively affected sentiment. Weakness across other grain and oilseed markets frequently translates into additional selling pressure in the wheat market. Importantly, the deteriorated condition of U.S. crops following earlier drought stress is currently insufficient to alter the prevailing trend. Investors remain focused primarily on the global supply picture, where production prospects in many other countries remain favorable, reinforcing expectations of abundant supplies in the months ahead. Corn harvesting is accelerating in Brazil, improving the overall supply outlook for feed grains. Demand for U.S. wheat remains weak, while importers continue to favor cheaper supplies from the Black Sea region. Additional pressure comes from recent data on crop conditions and global production prospects. Weather conditions across the U.S. Wheat Belt have improved yield expectations, encouraging further selling across grain markets. Although the latest USDA report showed U.S. crop conditions slightly weaker than a year ago, the market viewed these figures as insufficient to change the negative sentiment.

Prospects for global supply continue to play an increasingly important role, with higher exportable surpluses from Ukraine implying greater competition in world markets. In Australia, recent rainfall has improved conditions for wheat planting and encouraged late sowing activity, further supporting expectations for new-crop supply. Meanwhile, in Russia, the world’s largest wheat exporter, export prices remain stable due to the strong ruble and limited farmer selling, although analysts expect export shipments to decline in June. As a result, the market is increasingly focused on the prospect of ample global supply combined with weak demand for U.S. grain. This fundamental backdrop remains the primary argument supporting continued downside pressure on wheat prices in the coming weeks. From a technical perspective, the daily WHEAT chart shows a downside breakout from an ascending price channel, with prices falling below the 600 level. We recommend opening a short position on WHEAT with a take-profit target at 567 and a stop-loss at 620.

WHEAT (D1 timeframe)

Source: xStation5