EUR /

EUR /  USD — Euro / US Dollar

USD — Euro / US Dollar JPY — US Dollar / Japanese Yen

JPY — US Dollar / Japanese Yen GBP /

GBP /  AUD /

AUD /  CAD — US Dollar / Canadian Dollar

CAD — US Dollar / Canadian Dollar CHF — US Dollar / Swiss Franc

CHF — US Dollar / Swiss Franc NZD /

NZD / TSMC delivers a record quarter. AI is driving results and reshaping the entire cycle

- April 16, 2026

- Posted by: Today Markets

- Categories: Competitive research, Markets, Technical Analysis, Trading Indices

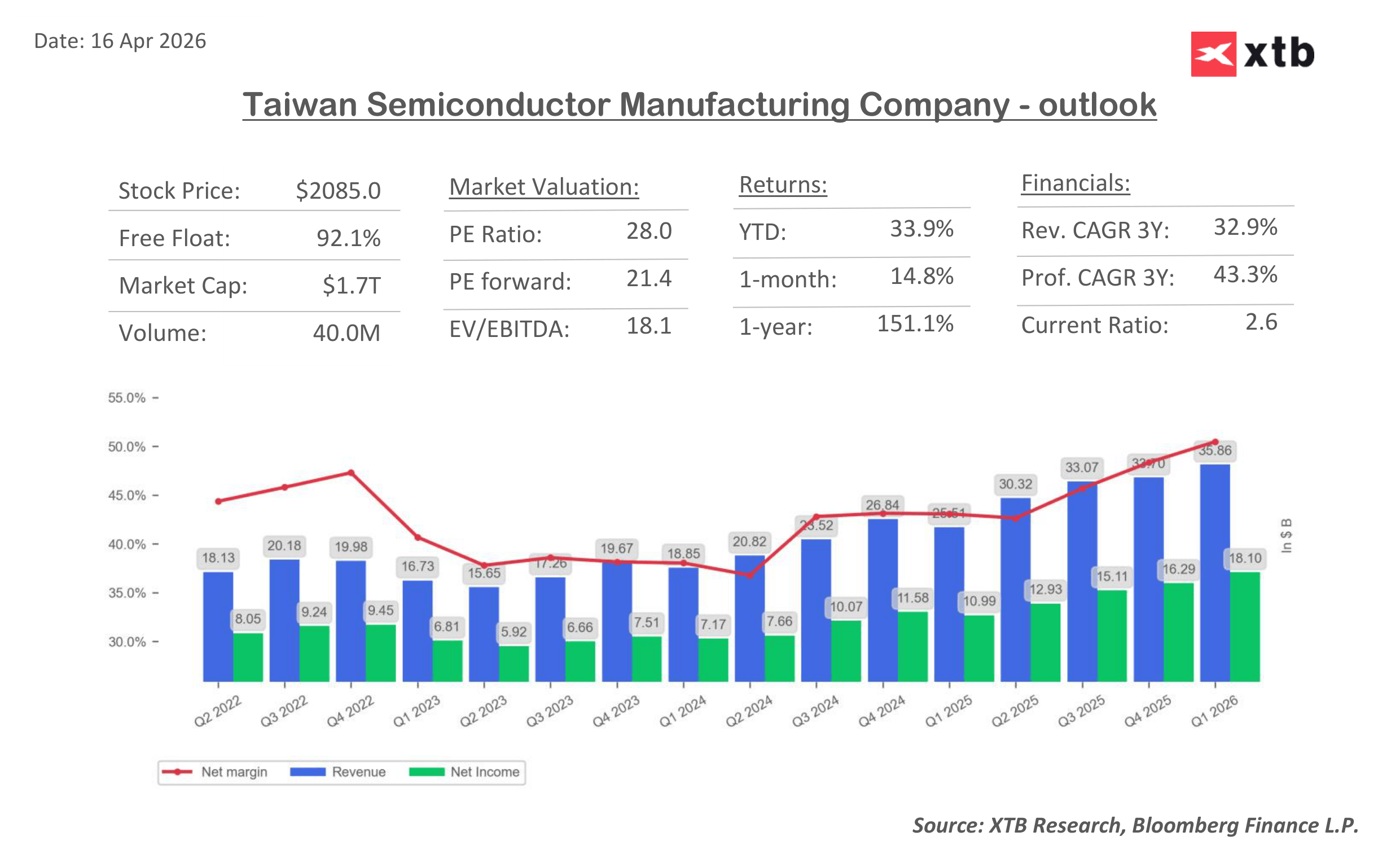

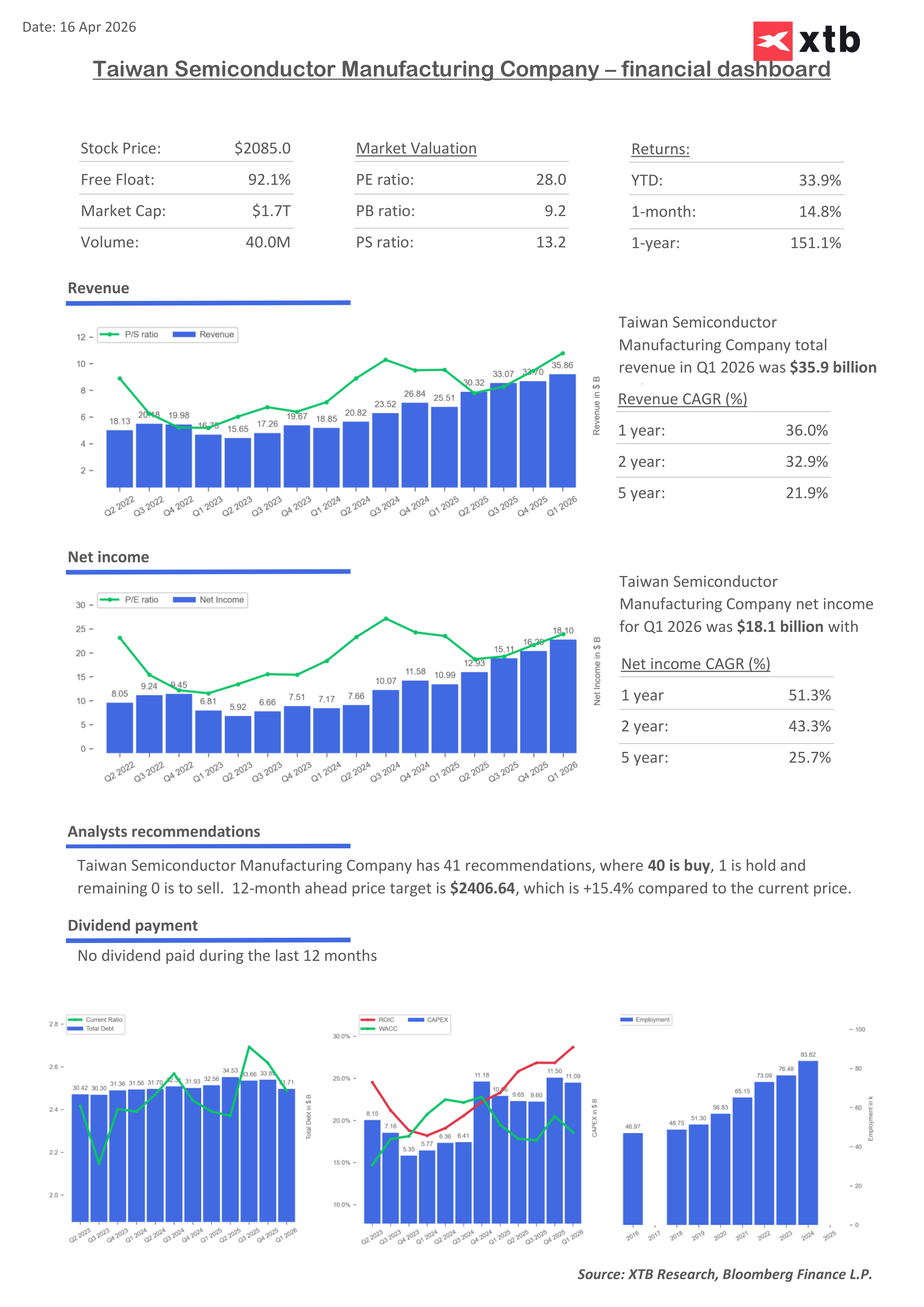

TSMC kicked off 2026 with a record-breaking quarter, clearly beating analyst expectations while also raising its full-year outlook. This is a very strong signal that demand for AI-related chips remains durable, even in a more challenging macro and geopolitical environment. This does not look like a typical cyclical rebound. The report shows that AI infrastructure is becoming the foundation of growth for the entire semiconductor sector, with TSMC positioned right at the center of it. In the first quarter, the company generated approximately $18.2 billion in net income, up 58% year over year, on revenue of $35.9 billion, up 41% year over year in USD terms. At the same time, profitability exceeded expectations, with gross margin at 66.2% and operating margin at 58.1%. Key financial highlights

- Revenue: $35.9 billion (+41% year over year in USD)

- Net income: $18.2 billion (+58% year over year)

- Operating income: approximately $20.9 billion (+62% year over year)

- Gross margin: 66.2%

- Operating margin: 58.1%

- Q2 revenue guidance: $39–40.2 billion

- Full-year 2026 revenue growth: above 30% year over year in USD

- 2026 capex: $52–56 billion (upper end of range)

Growth is one thing, but quality stands out The most important aspect of the report is not just the growth rate, but the structure of the results. TSMC is demonstrating very strong conversion of revenue into profit, driven by its dominance in leading-edge process technologies and the growing share of AI chips, which are among the most profitable segments in the market today. This is not a one-off effect. The revenue mix is shifting toward more advanced nodes and long-term contracts, improving visibility and margin stability. “Extremely strong demand” and tight capacity The key takeaway from the report is straightforward: demand continues to outpace supply. Management explicitly pointed to “extremely strong” demand for AI chips. Global leaders such as NVIDIA and AMD are developing increasingly advanced chips, directly driving demand for TSMC’s manufacturing capacity. The effect is structural. The market is operating under a shortage of leading-edge chips, where the main constraint is no longer demand, but the ability to supply it. The same trend is visible among equipment suppliers such as ASML. Strong outlook confirms sustained momentum Guidance for the second quarter reinforces this picture. TSMC expects revenue in the range of $39 to $40.2 billion, above market consensus, while maintaining very strong margins. The company also expects full-year 2026 revenue to grow by more than 30% year over year in USD terms. This is important because it shows that current momentum is not temporary, and demand is expected to remain strong in the coming quarters. Capex is rising for a reason This growth is supported by an aggressive investment strategy. TSMC plans capital expenditures of $52 to $56 billion, at the upper end of its previous guidance. The company is expanding capacity through new fabs, including major projects in the United States, to keep up with demand. This marks a key shift from previous cycles, where demand was the limiting factor. Today, the constraint is the ability to scale production.

Risks are present, but secondary to demand The company highlights geopolitical risks, including tensions in the Middle East, as well as currency effects on profitability. At the same time, it reports no significant disruptions in materials or energy supply, suggesting stable operations. At this stage, these risks appear secondary to very strong underlying demand. Conclusion: AI is reshaping the industry structure The first quarter of 2026 for TSMC is not just about strong results, but about confirming a deeper shift across the semiconductor industry. Artificial intelligence is becoming the primary driver of growth, rather than just one of many factors. In this environment, TSMC is in a uniquely advantaged position as the leading manufacturer of the world’s most advanced chips. If current trends persist, the company may operate in a multi-year cycle of strong demand, rising revenues, and solid profitability. The biggest challenge will not be finding customers, but keeping up with the scale of their demand.

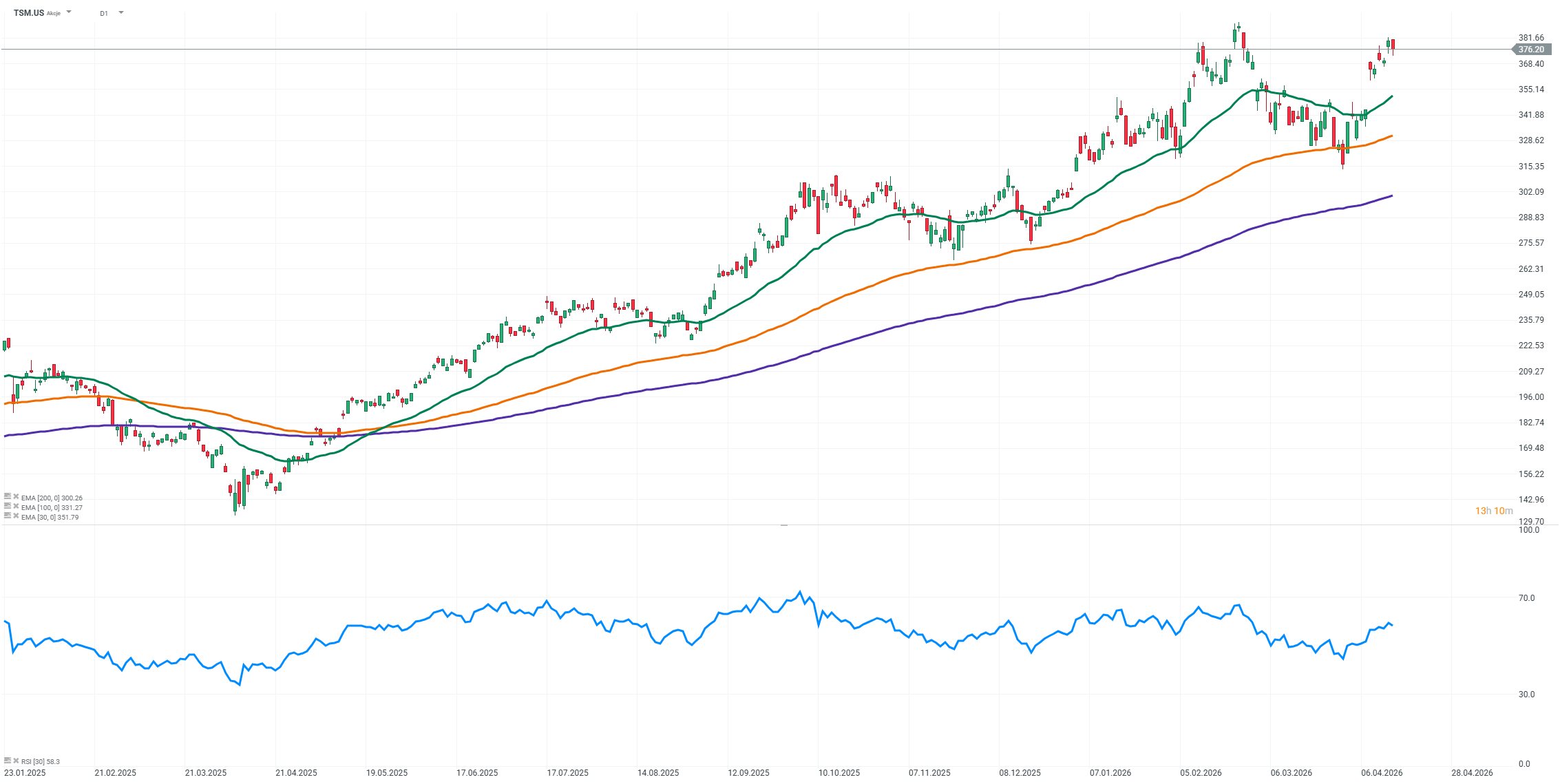

Souce: xStation5